Baro 10 xeelado dhaqaale oo wax ku ool ah oo kaa caawinaya inaad si xikmad leh u maareyso kharashaadka Ramadan, u qorshayso zakada, u kaydsato Ciidda, una dhisto mustaqbal maaliyadeed oo xasilloon.

Dad badan waxay u arkaan Ramadan bil kharash oo keliya. Laakiin marka si cilmi iyo qorshe leh loo eego, Ramadan waa fursad dahabi ah oo lagu hagaajin karo dhaqaalaha qoyska.

Anigoo ku hadlaya aragti dhaqaale oo qoto dheer, waxaan kuu soo bandhigayaa xeelado aad ku maareyn karto lacagtaada si aad uga baxdo bisha adigoo:

Qorshaha wanaagsan ma bilaabmo maalinta 1-aad ee Ramadan – wuxuu bilaabmaa ugu yaraan 30 maalmood ka hor.

Samee:

Khaladka ugu weyn waa in la isku qaldo baahida iyo rabitaanka.

Baahi:

Rabitaan:

Qofka dhaqaale yaqaan wuxuu rabitaanka ka hormariyaa baahida.

Ha u dukaameysan si maalinle ah adigoo aan qorshe lahayn.

Samee:

Tani waxay yaraynaysaa:

Zakadu waa tiir dhaqaale iyo mid diini ah.

Si xeeladaysan u samee:

Qorshaynta zakada waxay ka hortagtaa culays maalmaha ugu dambeeya.

Ramadan gudaheeda:

Fursad ka dhig inaad kaydsato lacagtaas halkii aad ku bixin lahayd meel kale.

Tusaale:

Lacagtaas waxaad u isticmaali kartaa:

Ganacsiyadu waxay kordhiyaan xayeysiinta Ramadan.

Maskaxda ku hay:

Iibsiga ku salee baahi, ma aha xayeysiin.

Qorshaha Ciidda:

Tani waxay yaraynaysaa qiimo kordhin iyo cadaadis.

Ramadan waa waqti ku habboon in carruurta lagu baro:

Dhaqan dhaqaale oo wanaagsan wuxuu ka bilaabmaa guriga.

Is weydii:

Qiimeyntu waa furaha horumar dhaqaale.

Ramadan ma aha oo kaliya bil cibaado; waa bil lagu dhiso edbin dhaqaale.

Qofka:

Wuxuu ka baxaa bisha isagoo dhaqaale ahaan ka xoog badan sidii hore.

—

16. Behavioral Finance: How Your Mind Affects Money Decisions.

Money Is Emotional Before It Is Logical

Many people think financial decisions are purely about numbers and calculations. In reality, emotions play a major role in how people manage money.

The most common emotions that damage financial progress are:

Fear

Impatience

Greed

Comparison

Regret

People who build long-term wealth are not smarter—they are better at controlling emotions.

—

17. Common Financial Mistakes Most People Make

1. Making Decisions Too Quickly

Impulse spending, rushed investments, and unplanned loans often lead to regret.

Solution:

Give yourself time. Even waiting 24 hours can prevent bad decisions.

—

2. Relying on Only One Source of Income

When your income depends on a single source, your financial stability is fragile.

Solution:

Consider:

Side income

Small businesses

Investments

Digital skills

—

3. Fear of Starting

Many people delay financial action while waiting for the “perfect time.”

Truth:

The best time to start improving your finances is now.

—

18. The Importance of Side Income

Why Side Income Matters

Side income:

Reduces financial pressure

Increases flexibility

Accelerates wealth-building

Even small, consistent extra income can make a huge difference over time.

Examples of Side Income

Freelancing

Blogging

Online teaching

E-commerce

Content creation

—

19. Managing Money When Income Increases

Higher Income Does Not Equal Wealth

Many people increase spending as soon as their income rises.

Wealth builders follow a different rule:

1. Increase savings first

2. Increase investments second

3. Improve lifestyle last

—

20. The Importance of Financial Goals

Without Goals, Money Disappears

Money without direction gets wasted.

Effective financial goals are:

Clear

Measurable

Time-based

Example: ❌ “I want more money”

✅ “I want to save $10,000 within three years”

—

21. Separating Needs From Wants

Needs vs. Wants

Needs include:

Food

Shelter

Healthcare

Education

Wants include:

Luxury items

Expensive upgrades

Non-essential entertainment

Long-term wealth comes from prioritizing needs before wants.

—

22. Family, Environment, and Financial Influence

Your Environment Shapes Your Financial Behavior

If you are surrounded by people who:

Overspend

Avoid planning

Mock saving

Financial progress becomes harder.

Solution:

Surround yourself with people who value:

Growth

Discipline

Long-term thinking

—

23. The Power of Patience

Patience Is a Financial Asset

Wealth does not appear in:

One month

One year

One decision

It grows through:

Time

Consistency

Patience

—

24. Investment Mistakes to Avoid

Avoid:

Investing in things you don’t understand

Following others blindly

Chasing quick profits

Selling during market fear

Successful investors:

Stay calm

Think long-term

Trust their plan

—

25. Automating Your Financial System

Why Automation Works

Automation removes emotion and inconsistency.

You can automate:

Savings

Investments

Bill payments

This creates:

Fewer mistakes

Better discipline

Lower stress

—

26. Building Generational Wealth

What Is Generational Wealth?

Generational wealth is financial security that:

Lasts beyond your lifetime

Supports your children and family

Creates long-term opportunity

It requires:

Planning

Education

Responsible habits

—

27. Risk Management and Future Planning

Lack of Planning Is the Biggest Risk

Life is unpredictable.

A strong financial plan prepares for:

Health emergencies

Job loss

Economic changes

Preparation protects progress.

—

28. One Smart Decision Every Day

Small Decisions Create Big Change

You don’t need to change everything at once.

Start with:

One habit

One saving goal

One improvement

Consistency matters more than perfection.

—

Conclusion (Part 2)

Long-term wealth is not built through luck or sudden success. It is built through daily financial decisions, emotional control, patience, and discipline.

Anyone—regardless of current income—can move toward financial stability and freedom by making smarter choices every day.

—

Practical Money Skills for Budgeting, Saving, Investing & Financial Freedom|

By Dhilaalo.com

Introduction:

Why Personal Finance Matters More Than Ever.

In today’s fast-changing world, personal finance is no longer a topic reserved for economists, bankers, or wealthy investors. It has become a daily survival skill for everyday people. From managing monthly expenses to planning long-term financial security, understanding how money works directly affects the quality of our lives.

Rising living costs, unstable global markets, inflation, digital currencies, and online financial tools have changed how people earn, spend, save, and invest money. Many people work hard every day, yet still struggle financially—not because they don’t earn enough, but because they were never taught how to manage money intelligently.

This guide was created to solve that problem.

At Dhilaalo.com, we believe personal finance should be simple, practical, and accessible to everyone—regardless of income level, education, or background. This article breaks down complex financial concepts into clear, real-world strategies that everyday people can apply immediately.

By the end of this guide, you will understand:

How to control your money instead of chasing it

How to build a realistic budget that actually works

How to save consistently, even on a low income

How investing works and how beginners can start safely

How to reduce financial stress and move toward long-term freedom

1. Understanding Personal Finance: The Foundation

Personal finance is the management of an individual’s or household’s money.

It includes:

Income management

Spending decisions

Saving habits

Investing strategies

Risk protection (insurance & emergency planning)

At its core, personal finance answers one key question:

How do I make my money work for me instead of working forever for money?

The Five Pillars of Personal Finance

Income

Budgeting

Saving

Investing

Financial Protection & Planning

Ignoring even one of these pillars creates financial instability.

2. Budgeting: Taking Control of Your Money

What Is a Budget?

A budget is a plan for your money, not a punishment. It tells your money where to go instead of wondering where it went.

Why Most Budgets Fail

Unrealistic expectations

Over-restriction

No flexibility

No tracking system

The 50/30/20 Rule (Beginner Friendly)

50% → Needs (rent, food, bills)

30% → Wants (entertainment, lifestyle)

20% → Savings & investments

If your income is low, adjust the percentages—but always save something.

Zero-Based Budgeting

Every dollar is assigned a job: Income − Expenses − Savings = 0

This method gives maximum control and awareness.

3. Saving Money: Building Financial Security

Why Saving Is Non-Negotiable

Savings protect you from:

Emergencies

Debt traps

Financial stress

Poor decisions under pressure

Emergency Fund

Your first goal:

3–6 months of living expenses

Kept in an accessible account

Used only for real emergencies

Saving on a Low Income

Save before spending

Automate savings

Start small (even $1/day matters)

Increase savings when income increases

Consistency matters more than amount.

4. Debt Management: Escaping the Debt Cycle

Good Debt vs Bad Debt

Good Debt

Education

Business

Income-producing assets

Bad Debt

High-interest consumer debt

Credit cards for lifestyle spending

Debt Snowball Method

Pay smallest debt first

Gain motivation

Roll payments forward

Debt Avalanche Method

Pay highest interest first

Saves more money long-term

Choose the method that keeps you consistent.

5. Investing: Making Money Grow Over Time

What Is Investing?

Investing means putting money into assets that grow in value or generate income over time.

Why Investing Is Essential

Saving protects money. Investing multiplies money.

Beginner Investment Options

Index funds

Mutual funds

Stocks

Real estate

Bonds

ETFs

Digital assets (with caution)

Power of Compound Interest

Money grows faster when profits are reinvested.

Time in the market beats timing the market.

6. Personal Finance in the Digital Age

Online Banking & Fintech

Mobile banking

Budgeting apps

Investment platforms

Crypto exchanges

Benefits

Accessibility

Transparency

Speed

Automation

Risks

Scams

Over-trading

Lack of regulation

Financial education is your best protection.

7. Building Multiple Income Streams

Relying on one income source is risky.

Common Income Streams

Salary

Freelancing

Online businesses

Investments

Digital content

Passive income assets

Multiple streams increase financial stability.

8. Financial Freedom: What It Really Means

Financial freedom does not mean being rich. It means:

Freedom of choice

Reduced stress

Control over time

Ability to handle emergencies

Steps Toward Financial Freedom

Control spending

Eliminate bad debt

Build savings

Invest consistently

Increase income

Protect assets

9. Common Personal Finance Mistakes

Living without a budget

Ignoring savings

Emotional spending

Chasing quick profits

Avoiding financial education

Awareness is the first step to correction.

10. Personal Finance for Everyday People (Reality-Based Advice)

This guide is not about luxury lifestyles. It is about:

Practical decisions

Small consistent actions

Long-term thinking

You don’t need to be rich to manage money well. You need discipline, knowledge, and patience.

Conclusion: Take Control of Your Financial Future

Personal finance is not about perfection. It is about progress.

Every small step you take today creates a stronger financial future tomorrow. Whether you are just starting or rebuilding, the most important step is starting now.

At Dhilaalo.com, our mission is to make financial knowledge accessible, practical, and empowering for everyday people.

Your money journey starts with understanding—and this guide is your first step.

Most people believe that wealth is created through big moments—landing a high-paying job, starting a successful business, or making a lucky investment. In reality, long-term wealth is built through small, everyday financial decisions repeated consistently over time.

Every choice you make about money—how you spend, save, borrow, invest, and protect it—shapes your financial future. These decisions may seem insignificant on a daily basis, but when combined over months and years, they determine whether you struggle financially or build lasting wealth.

This article is written for everyday people. You do not need to be wealthy, highly educated, or financially experienced. You only need awareness, discipline, and a willingness to improve one decision at a time.

—

1. Understanding Wealth as a Process, Not a Destination

Wealth Is Built Slowly

True wealth does not happen overnight. It is the result of:

Consistent habits

Long-term thinking

Patience

Discipline

People who chase quick money often lose it just as fast. Those who focus on systems and habits tend to build sustainable wealth.

Financial Freedom vs. Richness

Being wealthy does not always mean being rich. Financial freedom means:

You can meet your needs comfortably

You are not constantly stressed about money

You have options and flexibility

Your money supports your life goals

Everyday financial decisions are what move you toward that freedom.

—

2. The Power of Daily Spending Decisions

Small Expenses Matter More Than You Think

Many people ignore small daily expenses:

Coffee

Snacks

Subscriptions

Impulse purchases

While each cost may be small, together they can drain thousands of dollars annually.

Wealthy individuals are not cheap—they are intentional.

Conscious Spending

Ask yourself:

Do I need this?

Does this align with my goals?

Is this a habit or a choice?

Controlling spending does not mean suffering. It means directing money toward what truly matters.

—

3. Budgeting as a Tool for Control, Not Restriction

Why Budgeting Is Essential

A budget is not a punishment. It is a plan.

Budgeting helps you:

Understand where your money goes

Prevent overspending

Save intentionally

Reduce stress

Make confident decisions

People who avoid budgeting often feel confused and anxious about money.

Simple Budget Structure

A basic budget includes:

Income

Fixed expenses

Variable expenses

Savings

Investments

You do not need complex spreadsheets. Clarity is more important than perfection.

—

4. Saving: The Foundation of Financial Security

Why Saving Comes Before Investing

Saving provides:

Emergency protection

Stability

Confidence

Without savings, one unexpected expense can destroy progress.

Emergency Funds

An emergency fund should cover:

3–6 months of living expenses

Medical emergencies

Job loss

Unexpected repairs

This fund is not for luxury—it is for survival and peace of mind.

—

5. The Psychological Impact of Financial Stability

Reduced Stress

People with savings:

Sleep better

Make clearer decisions

Take fewer emotional risks

Financial stress affects:

Health

Relationships

Productivity

Mental well-being

Everyday saving decisions protect more than your money—they protect your life quality.

—

6. Managing Debt Wisely

Not All Debt Is Equal

There are two main types:

Bad debt (high interest, consumer debt)

Strategic debt (education, business, assets)

Uncontrolled debt destroys wealth slowly.

Everyday Debt Decisions

Ask:

Is this debt necessary?

Can I afford the repayments?

What is the interest cost over time?

Avoid debt that does not increase your long-term value.

—

7. Investing as a Long-Term Habit

Investing Is Not Gambling

True investing is:

Long-term

Diversified

Patient

Based on fundamentals

Short-term speculation often leads to losses.

Start Small

You do not need large capital to begin investing. The habit matters more than the amount.

Consistent investing builds wealth through compounding.

—

8. Compounding: The Hidden Force Behind Wealth

Time Is Your Greatest Asset

Compounding means:

Your money earns returns

Those returns earn returns

Growth accelerates over time

The earlier you start, the more powerful compounding becomes.

Even small amounts grow significantly with time and consistency.

—

9. Protecting Wealth Through Risk Management

Why Protection Matters

Wealth is not only about growth—it is also about protection.

Unexpected events can destroy years of effort without preparation.

Insurance and Planning

Basic protection includes:

Health insurance

Life insurance (if you have dependents)

Emergency planning

Protection allows wealth to survive crises.

—

10. Financial Discipline and Consistency

Motivation Fades, Discipline Lasts

Most people fail financially not due to lack of knowledge, but due to lack of discipline.

Daily discipline includes:

Tracking spending

Saving regularly

Avoiding emotional decisions

Staying focused on long-term goals

Small disciplined actions create big results.

—

11. Aligning Money With Life Goals

Money Is a Tool, Not the Goal

Ask:

What kind of life do I want?

What does financial success mean to me?

When money aligns with purpose, decisions become clearer and easier.

—

12. Avoiding Lifestyle Inflation

The Silent Wealth Killer

As income increases, many people increase spending immediately.

True wealth builders:

Increase savings first

Invest the difference

Maintain controlled lifestyles

Lifestyle inflation keeps people broke despite higher income.

—

13. Learning Financial Literacy Continuously

Knowledge Protects Wealth

Financial education helps you:

Avoid scams

Make better decisions

Adapt to change

Use tools wisely

Learning should be ongoing, not one-time.

—

14. Technology and Smart Financial Tools

Use Tools, Don’t Depend on Them

Apps and platforms help with:

Tracking

Automation

Analysis

But understanding fundamentals is more important than tools.

—

15. Building Wealth With Patience

Wealth Takes Time

Most overnight success stories hide years of effort.

Consistency beats intensity.

Focus on progress, not perfection.

—

Conclusion (Part 1)

Long-term wealth is built through everyday financial decisions, not rare opportunities. Each small choice either moves you closer to or further from financial freedom.

By controlling spending, saving consistently, managing debt wisely, investing patiently, and protecting your resources, you build a system that supports long-term success.

—

Financial wealth is not something that happens overnight. It is not a result of luck, inheritance, or secret knowledge known only by a few people. Financial wealth is built through clear understanding, disciplined behavior, and consistent action over time.

Many people work hard their entire lives yet remain financially stressed. Others, with similar or even lower income, manage to build stability, freedom, and wealth. The difference is not income alone—it is how money is managed.

This article explains, in clear and practical terms, the steps that help everyday people move toward financial wealth. These steps are not shortcuts. They are proven principles that work across countries, cultures, and income levels.

Before discussing steps, it is important to clarify what financial wealth actually is.

Financial wealth does not simply mean being rich. It means:

True financial wealth combines stability, security, and growth. It allows you to live with confidence today while preparing for tomorrow.

The journey toward financial wealth always begins with awareness.

Many people avoid looking closely at their finances because it feels uncomfortable. They do not track expenses, review income, or calculate debt. This lack of awareness creates confusion and poor decision-making.

Financial awareness means knowing:

When you understand these things clearly, money stops being a mystery and becomes a tool.

Without awareness:

With awareness:

Awareness does not require perfection—it requires honesty.

Spending less than you earn is the foundation of financial wealth. No amount of investing or financial knowledge can compensate for consistently spending more than income.

This principle sounds simple, but it requires discipline and planning.

Living within your means does not mean living poorly. It means:

When expenses are controlled, money begins to work for you instead of against you.

A budget is not a restriction—it is a plan. It tells your money where to go instead of wondering where it went.

A good budget:

Budgeting is not about cutting joy—it is about protecting your future.

One of the biggest reasons people fall into debt is unexpected expenses.

Emergencies are not rare events. They are part of life:

An emergency fund is money set aside specifically to handle these situations.

Without an emergency fund:

With an emergency fund:

Even saving a small amount consistently builds protection over time.

Debt is not always bad, but unmanaged debt is dangerous.

High-interest debt, emotional borrowing, and unnecessary loans prevent wealth creation. They drain income and limit flexibility.

Not all debt is equal:

The goal is not to fear debt, but to control it.

Reducing debt increases cash flow, confidence, and freedom.

Saving is the bridge between income and security.

Many people wait to save “when income increases.” In reality, saving should start immediately—even in small amounts.

Saving consistently:

Saving is not about how much you start with—it is about continuing.

Savings can serve different purposes:

Each type supports financial peace and resilience.

Saving protects money, but investing grows it.

Investing allows money to work for you over time through compounding. Wealth is rarely built through sudden gains—it is built through patient growth.

Investment success depends more on discipline than intelligence.

The earlier you invest, the more time works in your favor. Compounding rewards patience and consistency.

Financial education is a lifelong process.

The financial world changes:

People who continue learning avoid common mistakes and adapt more easily.

You do not need to be an expert. You need to understand the basics well.

Money decisions are often emotional, not logical.

Fear, excitement, pressure, and comparison lead to poor financial choices. Behavioral discipline is one of the strongest predictors of financial success.

Emotional control protects long-term goals.

Financial wealth is not built quickly.

Short-term thinking leads to:

Long-term thinking encourages:

Progress may feel slow, but consistency compounds results.

Money is a tool—not a purpose.

Financial wealth becomes meaningful when aligned with life goals such as:

When money serves clear goals, motivation increases and discipline strengthens.

These steps work because they:

Financial wealth is accessible to anyone willing to practice discipline and patience.

Understanding mistakes helps avoid them:

Avoiding these mistakes accelerates progress.

There is no final moment where financial learning ends. Wealth is maintained through:

Each step builds on the previous one.

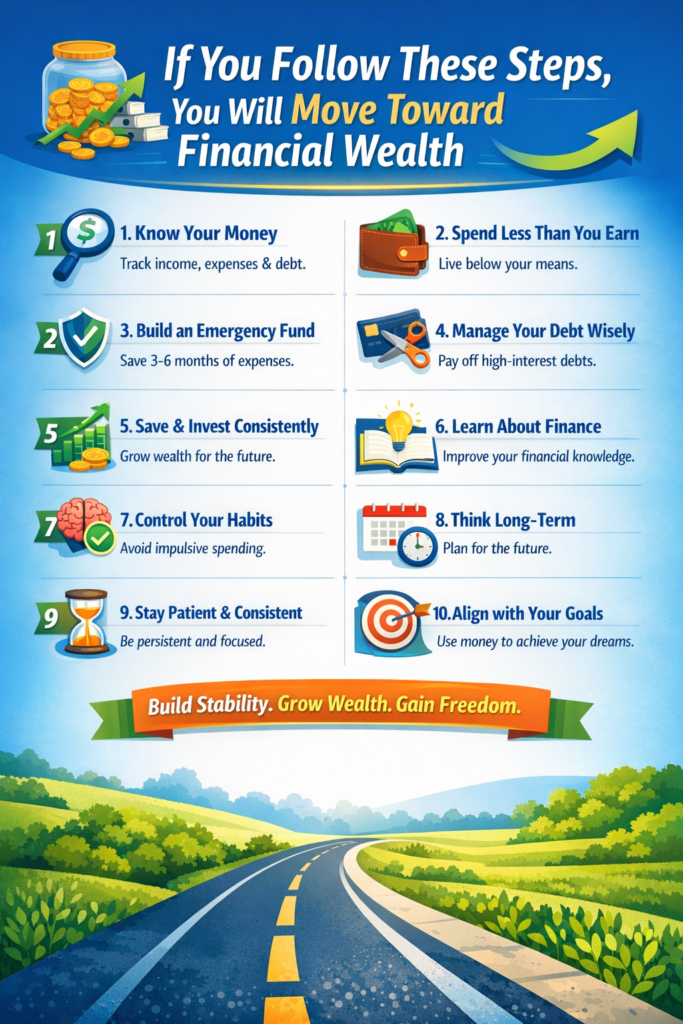

If you follow these steps, you will move toward financial wealth.

The journey requires effort, patience, and consistency—but it is achievable. Financial wealth is not about perfection. It is about direction.

By understanding money, managing behavior, planning for the future, and staying disciplined, anyone can build financial stability and long-term wealth.

Have you ever wondered why some people seem to build wealth effortlessly while others struggle financially despite earning the same income? The answer often isn’t income—it’s habits. Small daily decisions, repeated over time, can either create financial freedom or trap you in debt and missed opportunities.

In this post, we’ll explore three of the most common dangerous financial habits and how to break them.

Overspending is one of the most destructive financial habits. At first, it may seem harmless, but consistently spending more than you earn or failing to plan expenses can slowly erode wealth. People who overspend often live paycheck to paycheck—even with a decent salary.

Psychologists define overspending as spending driven by emotions or social pressures, not necessity. One splurge is fine, but consistent overspending—especially on non-essential items—creates a silent financial drain over time.

Fact: Over 60% of Americans admit to spending money they don’t have on unnecessary purchases, leading to an average credit card debt of $6,000 per household.

Why do people overspend?

Tip: Keep a spending journal for 30 days. Track every purchase, why you made it, and how it made you feel. Awareness is the first step toward change.

Neglecting savings is a silent financial killer. Without a cushion, emergencies—like medical bills, car repairs, or job loss—can spiral into debt and stress.

Statistic: Nearly 40% of Americans cannot cover a $400 emergency without borrowing.

Ignoring savings also limits opportunities for investment, education, or business ventures. Every day spent not saving is a missed opportunity to grow wealth.

Social and cultural pressures to spend rather than save also make it difficult to prioritize financial security.

Starting to save early allows your money to grow exponentially through compound interest.

Example:

The 10-year head start almost doubles Sarah’s savings.

Psychological Benefits: Reduces stress, creates control, and enables flexibility for opportunities.

Credit is a tool—but overreliance can destroy wealth. Many people use credit cards, loans, or buy-now-pay-later schemes to maintain lifestyles beyond their means. Over time, high-interest debt mounts, limiting financial growth.

Fact: The average American credit card debt is $5,000, with 40% carrying balances month-to-month.

Excessive credit use often hides a deeper problem: lack of budgeting and discipline. The “buy now, pay later” mindset creates an illusion of security while debt quietly accumulates.

Example: $10,000 credit card debt at 20% interest → $20,000 lost in 10 years if unpaid.

Case Study: Michael had $25,000 credit card debt → eliminated in 3 years using strict budgeting → invested savings → net worth $100,000 by 35.

✅ Key Takeaways from These 3 Habits

Breaking these habits is not about income—it’s about behavior, awareness, and discipline. Small changes today compound into massive financial results tomorrow.

Personal finance is one of the most important life skills, yet one of the least taught. Many people earn money every month, but only a few truly understand how to manage it, grow it, and use it to create long-term financial security. This guide explores personal finance mastery in a clear, practical, and actionable way—helping you take control of your money and build a financially independent future.

Whether you are just starting your financial journey or looking to refine your strategies, this article will walk you through smart money management, proven investing principles, and the mindset required to achieve financial freedom.

What Is Personal Finance and Why It Matters

Personal finance refers to how individuals earn, spend, save, invest, and protect their money. It affects nearly every part of life—where you live, the opportunities you can pursue, your stress levels, and your long-term security.

Without financial literacy, many people fall into common traps:

Living paycheck to paycheck

Accumulating high-interest debt

Lacking savings for emergencies

Making emotional investment decisions

With personal finance mastery, however, money becomes a tool, not a source of stress. You gain clarity, confidence, and the ability to plan for both short-term needs and long-term goals.

Smart Money Management: Building Strong Financial Habits

Understanding Cash Flow

At the core of personal finance is cash flow—the relationship between income and expenses. Positive cash flow means you earn more than you spend. Negative cash flow keeps you trapped financially, no matter how much you earn.

Tracking income and expenses is the first step toward financial control. Once you understand where your money goes, you can make informed decisions instead of reacting impulsively.

Budgeting Without Feeling Restricted

Budgeting is often misunderstood as limiting or boring. In reality, a good budget gives freedom. It ensures your money is aligned with your priorities.

Effective budgeting strategies include:

Allocating money to essentials first

Saving automatically

Setting aside guilt-free spending money

Reviewing and adjusting monthly

A budget should support your lifestyle, not punish it.

Expense Management That Makes Sense

Smart financial management is not about cutting everything—it’s about spending intentionally. Reducing unnecessary expenses creates room for savings and investments without lowering quality of life.

Ask yourself:

Does this expense add long-term value?

Is it aligned with my goals?

Can I get the same value for less?

Saving Money and Preparing for the Unexpected

Saving money creates stability. It protects you from unexpected events like medical emergencies, job loss, or economic downturns.

A solid financial foundation includes:

An emergency fund (3–6 months of expenses)

Short-term savings for planned goals

Long-term savings for future investments

Saving works best when it’s automatic and consistent. Treat savings as a fixed expense, not what’s left over.

Debt Management and Credit Awareness

Debt can either help or harm your financial life. Understanding the difference is crucial.

Productive vs Harmful Debt

Productive debt may increase income or long-term value, while harmful debt—especially high-interest consumer debt—drains wealth.

Smart debt management involves:

Paying off high-interest debt first

Avoiding lifestyle debt

Using credit strategically, not emotionally

Reducing debt increases financial flexibility and lowers stress.

Investing Strategies for Long-Term Growth

Saving alone is not enough. Inflation reduces the value of money over time, making investing essential for long-term wealth building.

Why Investing Matters

Investing allows your money to grow through compound returns. Over time, even small investments can turn into significant wealth when combined with patience and consistency.

Core Investing Principles

Successful investors focus on:

Long-term thinking

Diversification

Risk management

Consistent contributions

Investing is not about timing the market—it’s about time in the market.

Common Investment Options

Popular investment assets include:

Stocks and equity funds

Index funds and ETFs

Real estate

Bonds and fixed-income assets

A diversified portfolio balances growth potential with stability.

Financial Freedom: What It Really Means

Financial freedom means having enough income or assets to support your lifestyle without relying solely on active work. It’s not about extreme wealth—it’s about choice and independence.

People pursue financial freedom to:

Reduce stress

Gain time flexibility

Focus on meaningful work

Protect their families’ future

Building passive or semi-passive income streams accelerates this process.

The Role of Mindset in Financial Success

Personal finance is not just about numbers—it’s about behavior. Long-term success depends on discipline, patience, and emotional control.

Key mindset shifts include:

Thinking long-term instead of short-term

Valuing progress over perfection

Avoiding comparison with others

Viewing money as a tool, not a status symbol

Those who master their mindset often outperform those with higher incomes but poor habits.

Long-Term Planning and Wealth Protection

True financial mastery includes planning for the future and protecting what you build. Insurance, diversification, and strategic planning help safeguard years of progress from unexpected risks.

Long-term planning also involves thinking beyond yourself—how your financial decisions today impact your family and future generations.

Final Thoughts: Taking Control of Your Financial Future

Personal finance mastery is a journey, not a one-time decision. It requires learning, adjusting, and staying committed over time. The reward is financial clarity, reduced stress, and the freedom to make choices based on purpose—not pressure.

By managing money wisely, investing consistently, and thinking long-term, anyone can move closer to financial independence and lasting security.

🔑 Key Takeaway.

You don’t need to be rich to master personal finance.

You need knowledge, discipline, and consistency.

Introduction

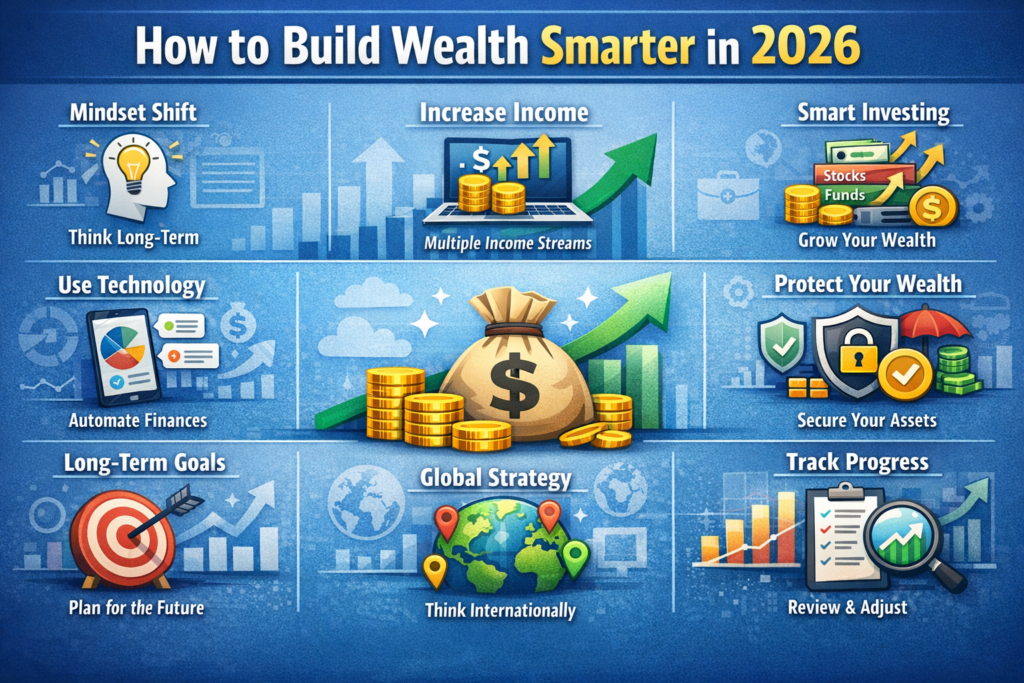

Building wealth in 2026 is no longer about working harder alone—it’s about working smarter. With rising inflation, fast-changing technology, global economic uncertainty, and new digital opportunities, smart wealth building requires strategy, discipline, and adaptability.

This guide is designed for everyday people who want clarity, not hype. Whether you’re starting from zero or rebuilding your finances, this article will help you understand how to grow, protect, and sustain wealth intelligently in 2026 and beyond.

Why 2026 Requires a Smarter Wealth Strategy

The financial world has changed dramatically in recent years. Traditional advice alone is no longer enough.

Key realities of 2026:

Inflation continues to reduce purchasing power

Digital finance and online income are mainstream

Job security is less predictable

Passive income is no longer optional—it’s essential

Smart wealth builders understand the system and position themselves ahead of it, not behind it.

1. Master Your Money Mindset First

Before money grows in your bank account, it grows in your thinking.

Smart mindset shifts for 2026:

From “saving leftovers” → to “paying yourself first”

From “quick money” → to “long-term systems”

From fear of investing → to educated risk management

Wealth is built by consistency, not luck.

2. Build a Strong Financial Foundation

You can’t build wealth on weak ground.

Essentials you must have:

A clear monthly budget

An emergency fund (3–6 months of expenses)

Zero or controlled high-interest debt

Rule of 2026:

If you don’t control your cash flow, you don’t control your future.

3. Increase Income Before You Over-Optimize Expenses

Cutting expenses helps—but income growth changes lives.

Smart income ideas in 2026:

Digital skills (AI tools, content, design, writing)

Freelancing platforms

Online businesses and blogs

Affiliate marketing

Remote and global work

The goal is multiple income streams, not dependency on one source.

4. Invest Smarter, Not Harder

Investing in 2026 is about ownership, not gambling.

Smart long-term investment options:

Index funds & ETFs

Dividend-paying stocks

Long-term stock ownership (not day trading)

Education and skill investments

Scalable digital assets

Smart investors think in years, not weeks.

5. Use Technology as a Wealth Tool

Technology is the biggest advantage of this generation.

Smart tech usage:

Budgeting and finance apps

Automated savings

Market tracking tools

Email newsletters and financial alerts

Online learning platforms

Those who ignore technology fall behind financially.

6. Protect Your Wealth Like a Professional

Growing money is only half the work—protecting it matters just as much.

Protection strategies:

Emergency savings

Diversified investments

Avoid emotional decisions

Digital security (passwords, 2FA)

Clear financial goals

Smart people plan for bad days before they arrive.

7. Focus on Long-Term Wealth, Not Lifestyle Pressure

Social media pushes spending. Smart people resist it.

Wealth builders:

Delay gratification

Invest before upgrading lifestyle

Value freedom over appearances

Choose assets over liabilities

True wealth is peace of mind, not public approval.

8. Create Systems, Not Willpower

Willpower fails. Systems work.

Smart systems include:

Automatic savings

Scheduled investing

Monthly financial reviews

Clear yearly goals

When money decisions are automated, mistakes decrease.

9. Think Globally, Act Strategically

2026 is a global financial era.

Smart individuals:

Learn international markets

Understand global trends

Follow reliable financial education platforms

Avoid financial misinformation

Knowledge is the highest-return investment.

10. Measure Progress, Adjust, Repeat

Wealth building is not linear.

Ask yourself regularly:

Is my net worth growing?

Are my skills improving?

Am I closer to financial freedom than last year?

Small adjustments today create massive results tomorrow.

What Smart Wealth Looks Like in 2026

Smart wealth is:

Sustainable

Flexible

Peaceful

Independent

It’s not about being rich fast—it’s about being free long-term.

Final Thoughts

2026 offers more financial opportunities than any previous generation—but only to those who prepare, learn, and act wisely.

If you focus on:

Education

Consistency

Smart investing

Long-term thinking

You won’t just survive financially—you’ll thrive.

About Dhilaalo.com

Dhilaalo.com is dedicated to helping individuals build smarter financial lives through education, strategy, and clarity—without hype or false promises.

Build wealth. Build freedom. Build smart.

Personal finance is not just about money—it is about control, freedom, and long-term security. In today’s uncertain economic environment, mastering personal finance has become one of the most valuable life skills anyone can develop. This comprehensive guide is designed to be a reference article you can return to repeatedly as your financial situation evolves.

Whether you are just starting your financial journey or looking to refine your existing strategy, this article will walk you through foundations, systems, habits, and advanced thinking that lead to financial stability and long-term wealth.

What Is Personal Finance and Why It Matters

Personal finance refers to how an individual earns, spends, saves, invests, and protects money over time. It is deeply connected to lifestyle choices, mindset, discipline, and long-term planning.

Personal Finance Is a Life Skill, Not a One-Time Decision

Many people believe financial success comes from a high income. In reality, it comes from how money is managed, not how much is earned. Without financial literacy, even large incomes disappear quickly.

Personal finance matters because it:

Reduces stress and anxiety

Creates long-term security

Allows freedom of choice

Protects against emergencies

Builds generational wealth

The Foundation of Strong Personal Finance

Before investing or growing wealth, you must build a solid financial foundation.

H3: Understanding Your Income Clearly

Income is the starting point of all financial decisions. You must know:

How much money you earn

How often you receive it

Whether it is stable or variable

Without clarity, budgeting and planning become impossible.

Tracking Expenses Without Emotion

Expense tracking is not about restriction—it is about awareness. Most people lose money not on big purchases, but on small, repeated expenses.

A strong personal finance system requires:

Categorizing expenses (needs vs wants)

Identifying financial leaks

Reviewing spending monthly

Budgeting as a Financial Control System

Budgeting is not punishment—it is permission to spend with confidence.

H3: Why Most Budgets Fail

Budgets fail because they are:

Unrealistic

Too restrictive

Not aligned with lifestyle

A successful budget adapts to real behavior, not ideal behavior.

Creating a Sustainable Budget

A strong budget should:

Cover essential needs

Allow flexibility

Include savings automatically

Adjust over time

Budgeting is a living system, not a fixed rule.

Saving Money as a Strategic Habit

Saving is not what remains after spending—it is what you prioritize first.

Emergency Funds as Financial Armor

An emergency fund protects you from:

Debt

Panic decisions

Financial setbacks

A healthy emergency fund typically covers 3–6 months of living expenses.

Automating Savings for Consistency

Automation removes emotion from saving. When savings happen automatically, discipline becomes effortless.

Debt Management and Financial Discipline

Debt can either be a tool or a trap.

Good Debt vs Bad Debt

Good debt:

Builds assets

Increases earning potential

Bad debt:

Funds consumption

Carries high interest

Understanding this distinction is critical.

Escaping the Debt Cycle

To reduce debt effectively:

Prioritize high-interest debt

Avoid lifestyle inflation

Maintain consistent payments

Debt freedom creates financial breathing space.

Investing for Long-Term Wealth

Saving protects money. Investing grows it.

H3: Why Investing Is Necessary

Inflation silently reduces purchasing power. Investing allows money to outpace inflation and grow over time.

Long-Term Thinking Over Short-Term Gains

Successful investing rewards:

Patience

Consistency

Emotional control

Wealth is built through time in the market, not timing the market.

Financial Mindset and Psychology

Money behavior is deeply psychological.

Scarcity vs Abundance Thinking

A scarcity mindset leads to fear-based decisions.

An abundance mindset focuses on growth, planning, and opportunity.

Delayed Gratification as a Wealth Skill

The ability to delay pleasure is one of the strongest predictors of financial success.

H2: Protecting Your Financial Future

Wealth building must include protection.

Insurance and Risk Management

Insurance protects against:

Health emergencies

Loss of income

Unexpected disasters

Planning for the Unexpected

Financial resilience comes from preparation, not prediction.

Building a Long-Term Personal Finance Strategy

Personal finance is not static.

H

Reviewing and Adjusting Regularly

Life changes—so must your financial strategy. Regular reviews keep plans aligned with reality.

Personal Finance as a Lifetime System

The goal is not perfection.

The goal is progress, control, and peace of mind.

Final Thoughts on Personal Finance Mastery

Mastering personal finance is one of the most empowering decisions a person can make. It creates stability, confidence, and long-term freedom. This article is designed to serve as a reference point—something you revisit whenever you need clarity or direction.

True financial success is built slowly, intentionally, and sustainably.

Introduction

Many people want to invest but feel overwhelmed by market noise, fear of losses, and confusing advice online. The truth is that successful investing doesn’t require complex strategies or constant trading. Long-term investing is about patience, consistency, and discipline.

This guide explains how beginners can invest confidently for the long term, avoid common mistakes, and build wealth steadily over time—without stress or guesswork.

1. What Long-Term Investing Really Means

Long-term investing focuses on years and decades, not days or weeks. Instead of trying to time the market, long-term investors buy quality assets and hold them through market cycles.

Key benefits:

Lower stress

Fewer mistakes

Compound growth

Better tax efficiency

2. Why Long-Term Investing Works

Markets move up and down in the short term, but historically they trend upward over the long run. Time smooths volatility and rewards patience.

Core reasons it works:

Compound interest

Economic growth

Reinvestment of returns

Reduced emotional decisions

3. Start With Clear Financial Goals

Before investing, define your goals:

Retirement

Home purchase

Education

Financial independence

Clear goals determine:

Risk level

Time horizon

Asset allocation

4. Build a Solid Base Before Investing

Before investing:

Build an emergency fund

Eliminate high-interest debt

Create a basic budget

This protects your investments from forced withdrawals during emergencies.

5. Choose Beginner-Friendly Investments

For most beginners, simplicity wins.

Best options:

Index funds

ETFs

Broad market funds

Dividend-paying stocks (later)

Avoid complex or speculative assets early on.

6. The Power of Dollar-Cost Averaging

Dollar-cost averaging means investing a fixed amount regularly, regardless of market conditions.

Benefits:

Reduces timing risk

Builds discipline

Smooths market volatility

This strategy works especially well for long-term investors.

7. Diversification: Don’t Bet on One Thing

Diversification spreads risk across:

Industries

Markets

Asset classes

A diversified portfolio protects you from major losses if one sector underperforms.n

8. Avoid Common Investing Mistakes

Common mistakes to avoid:

Emotional trading

Chasing trends

Panic selling

Overconfidence

Ignoring fees

Successful investors focus on systems, not emotions.

9. Stay Invested During Market Downturns

Market crashes are normal. Selling during downturns often locks in losses.

What long-term investors do instead:

Stay invested

Continue contributions

Buy assets at lower prices

Downturns are opportunities, not disasters.

10. Review and Adjust Periodically

Long-term investing is not “set and forget” forever.

Review:

Once or twice per year

After major life changes

Adjust only when necessary—not based on emotions.

Conclusion

Long-term investing is one of the most reliable ways to build wealth. You don’t need perfect timing, expert predictions, or constant monitoring. What you need is clarity, consistency, and patience.

Start small. Stay disciplined. Let time work for you.

👉 Learn more simple investing and personal finance strategies at Dhilaalo.com