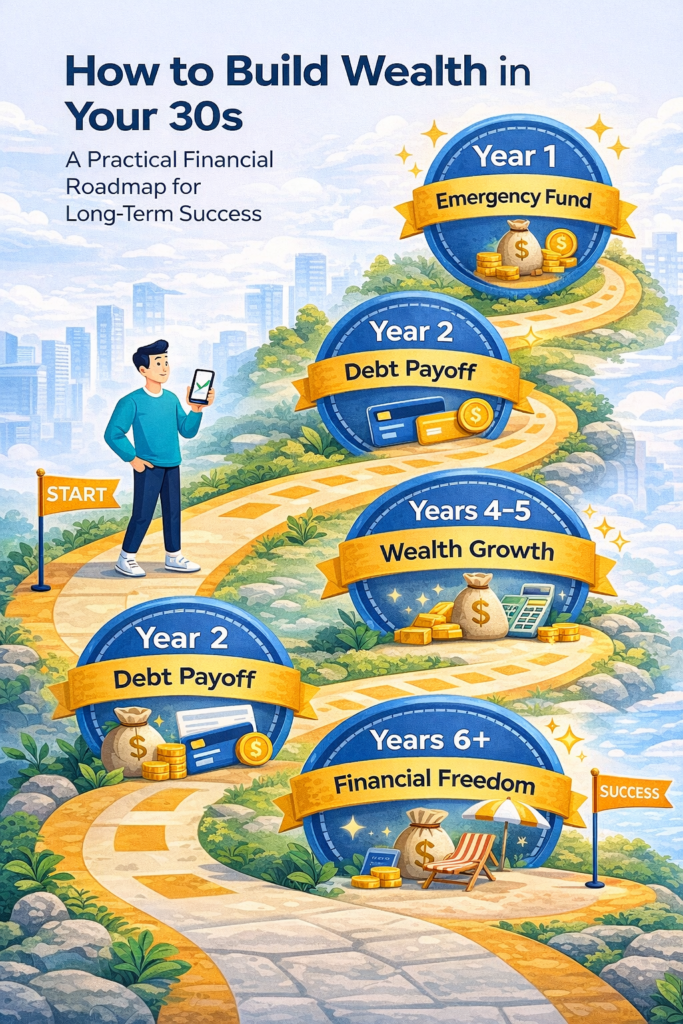

Introduction

Your 30s are one of the most powerful decades for building long-term wealth. You may be earning more than before, gaining career stability, or starting a family. But at the same time, expenses increase, responsibilities grow, and financial mistakes can become more costly.

The good news?

With the right strategy, your 30s can set you up for financial freedom in your 40s and beyond.

This guide breaks down clear, realistic, and proven steps to help you build wealth from where you are—without hype, risky shortcuts, or unrealistic promises.

1. Understand Your Financial Starting Point

Before building wealth, you must know exactly where you stand.

Key things to review:

Monthly income (after tax)

Fixed expenses (rent, utilities, insurance)

Variable spending (food, entertainment)

Total debt (credit cards, loans)

Current savings and investments

Create a simple net worth calculation:

Net Worth = Assets − Liabilities

This number gives you clarity—not judgment. Wealth building starts with awareness.

2. Build a Strong Emergency Fund First

An emergency fund is the foundation of financial stability.

Why it matters:

Prevents debt during emergencies

Protects investments from early withdrawal

Reduces stress and financial anxiety

How much should you save?

3–6 months of essential expenses

Keep it in a high-yield savings account

Easy access, but not easy spending

This fund is not an investment—it’s insurance for your financial life.

3. Eliminate High-Interest Debt Aggressively

High-interest debt is one of the biggest obstacles to wealth.

Focus on:

Credit cards

Payday loans

High-APR personal loans

Two proven methods:

Debt Avalanche: Pay highest interest first

Debt Snowball: Pay smallest balance first for motivation

Paying off high-interest debt gives you a guaranteed return—often better than any investment.

4. Invest Early and Consistently

Time is your greatest asset in your 30s.

Best long-term investment options:

Index funds (S&P 500, Total Market)

ETFs with low expense ratios

Retirement accounts (401(k), IRA, Roth IRA)

Key principles:

Invest monthly (dollar-cost averaging)

Focus on long-term growth

Avoid emotional trading

You don’t need perfect timing—you need consistency.

5. Maximize Retirement Accounts

Retirement investing is not optional—it’s essential.

Smart steps:

Contribute enough to get employer match

Increase contributions with every raise

Prioritize tax-advantaged accounts

Why it works:

Tax benefits compound over decades

Employer match = free money

Automatic investing builds discipline

The earlier you invest, the less you need to contribute later.

6. Increase Your Income Strategically

Saving alone won’t build wealth—you must grow income.

High-impact income strategies:

Improve high-value skills

Negotiate salary every 1–2 years

Build online income (blogs, freelancing, digital products)

Invest in income-producing assets

Your income is your wealth engine. Focus on scalable growth.

7. Avoid Lifestyle Inflation

As income increases, spending often rises faster.

Wealthy people do this differently:

Maintain simple lifestyle

Increase investments before spending

Spend intentionally, not emotionally

Ask yourself:

“Does this purchase move me closer to financial freedom?”

Control lifestyle inflation, and wealth accelerates.

8. Protect Your Wealth with Insurance

Risk management is part of wealth building.

Essential coverage:

Health insurance

Term life insurance (if dependents)

Disability insurance

Basic liability protection

Insurance protects your progress from setbacks you can’t predict.

9. Build Multiple Streams of Income

Relying on one income source is risky.

Examples:

Dividend-paying investments

Content websites (like Dhilaalo.com)

Affiliate marketing

Rental income

Digital assets

Multiple income streams create stability and faster growth.

10. Think Long-Term and Stay Disciplined

Wealth is built through habits, not luck.

Long-term mindset:

Avoid get-rich-quick schemes

Focus on systems, not shortcuts

Review finances quarterly

Stay patient during market cycles

Small consistent actions over time create extraordinary results.

Common Mistakes to Avoid in Your 30s

Waiting too long to invest

Ignoring retirement planning

Living paycheck to paycheck despite higher income

Taking excessive investment risks

Copying others without a plan

Avoiding mistakes is just as important as making smart moves.

Conclusion

Building wealth in your 30s is not about perfection—it’s about direction.

If you:

Control spending

Eliminate high-interest debt

Invest consistently

Increase income

Stay disciplined

You create a financial future that gives you freedom, security, and choices.

Start where you are. Improve one step at a time.

Your future self will thank you.

Introduction: Why Your Money Mindset Matters More Than Money Itself

Many people believe that wealth starts with a high income, a lucky investment, or being born into the right family. In reality, long-term financial success almost always begins somewhere else: your mindset.

Your money mindset is the set of beliefs, habits, and attitudes you have about earning, saving, spending, and investing money. If your mindset is weak, even a large income can disappear quickly. If your mindset is strong, even a small income can grow into real wealth over time.

In today’s economy—with inflation, rising living costs, job uncertainty, and fast-changing markets—changing your money mindset is no longer optional. It is essential.

This guide will show you how to reset your thinking, take control of your finances, and build wealth from zero—step by step, in a realistic and practical way.

—

What Is a Money Mindset?

A money mindset is how you think and feel about money, often shaped by:

Childhood experiences

Family beliefs

Culture and society

Past financial successes or failures

Some people grow up believing:

“Money is hard to get”

“Rich people are greedy”

“I’ll never be good with money”

Others believe:

“Money is a tool”

“I can learn financial skills”

“Wealth is built, not inherited”

These beliefs quietly guide your financial decisions every day.

—

Fixed Money Mindset vs Growth Money Mindset

Fixed Money Mindset

People with a fixed money mindset often:

Avoid learning about money

Fear investing

Live paycheck to paycheck

Believe wealth is only for “other people”

This mindset keeps people stuck financially.

Growth Money Mindset

People with a growth money mindset:

See money as a skill they can learn

Focus on long-term thinking

Invest in knowledge

Accept short-term sacrifices for long-term freedom

This mindset creates wealth over time.

—

Why Most People Stay Broke (Even With Income)

It’s not always low income that keeps people poor. Common reasons include:

No financial education

Emotional spending

Lifestyle inflation

Fear of investing

Lack of long-term planning

Without changing how you think, earning more money often leads to spending more money—not building wealth.

—

Step 1: Become Aware of Your Financial Reality

Before changing anything, you must know where you stand.

Ask yourself:

How much do I earn monthly?

How much do I spend?

Do I save anything?

Do I have debt?

Do I invest at all?

Many people avoid these questions because they feel uncomfortable. But clarity is power. You cannot improve what you refuse to measure.

—

Step 2: Redefine What Wealth Means to You

Wealth is not:

Luxury cars

Showing off online

Competing with others

True wealth is:

Financial peace

Freedom of choice

Low stress about money

Time control

When you define wealth correctly, your decisions change naturally.

—

Step 3: Stop Living for Today Only

One of the biggest mindset shifts is moving from short-term pleasure to long-term thinking.

Examples:

Spending $5 daily on small habits = thousands lost yearly

Saving and investing early = compound growth over decades

Wealth is built quietly, slowly, and consistently.

—

Step 4: Build Financial Discipline (Not Motivation)

Motivation is temporary. Discipline lasts.

Simple disciplined habits:

Pay yourself first

Track expenses weekly

Automate savings

Avoid impulse purchases

You don’t need extreme frugality—just consistency.

—

Step 5: Build an Emergency Fund (Mental Safety Net)

An emergency fund changes your mindset instantly.

Benefits:

Reduces stress

Prevents debt

Gives confidence

Improves decision-making

Start small:

$500 → $1,000 → 3–6 months of expenses

This fund protects your progress.

—

Step 6: Eliminate High-Interest Debt Strategically

Debt is one of the biggest mindset killers.

High-interest debt:

Credit cards

Payday loans

Consumer loans

These silently steal your future income.

Strategy:

List debts

Focus on highest interest first

Avoid new bad debt

Freedom from debt creates mental clarity.

—

Step 7: Learn How Money Grows (Compound Interest)

Compound interest is one of the most powerful forces in finance.

Simple idea: Money earns money → that money earns more money → repeat.

Starting early matters more than starting big.

Even small, consistent investments can outperform large late ones.

—

Step 8: Start Investing With a Long-Term Mindset

Investing is not gambling when done correctly.

Long-term investing focuses on:

Stocks

Index funds

ETFs

Real businesses

Ignore short-term noise. Focus on ownership and time.

—

Step 9: Increase Your Income Without Changing Your Lifestyle

Wealth grows fastest when:

Income increases

Lifestyle stays stable

Ways to increase income:

Learn digital skills

Freelancing

Side projects

Online businesses

Extra income invested wisely accelerates freedom.

—

Step 10: Surround Yourself With Financially Smart Content

Your environment shapes your mindset.

Consume:

Financial education

Long-term thinking content

Realistic success stories

Avoid:

Get-rich-quick schemes

Fake luxury culture

Emotional trading hype

What you consume daily becomes how you think.

—

Common Money Mindset Mistakes to Avoid

Waiting for “perfect timing”

Comparing your journey to others

Expecting fast results

Giving up too early

Wealth is boring before it becomes exciting.

—

How Long Does It Take to Change Your Money Mindset?

Mindset change happens in phases:

Awareness (weeks)

Habit change (months)

Identity shift (years)

The goal is not perfection, but progress.

—

Final Thoughts: Wealth Starts in the Mind

Changing your money mindset is the most important financial decision you will ever make.

You don’t need:

A rich background

A perfect economy

Huge starting capital

You need:

Clear thinking

Consistent habits

Long-term patience

Money follows mindset. Always.

—

Introduction: Why Your Money Mindset Matters More Than Your Income

Most people believe that earning more money is the key to financial success. In reality, mindset matters far more than income. Two people can earn the same salary, yet one builds wealth while the other struggles paycheck to paycheck. The difference isn’t luck—it’s how they think about money.

Your money mindset shapes every financial decision you make: how you spend, save, invest, and plan for the future. Without the right mindset, even high income won’t protect you from debt, stress, and poor money choices.

In this guide, you’ll learn how to change your money mindset using simple, practical habits that actually work over time. No complicated formulas, no get-rich-quick promises—just realistic steps to build lasting financial stability and confidence.

—

1. Understanding What a Money Mindset Really Is

A money mindset is the set of beliefs, attitudes, and emotions you associate with money. These beliefs often develop early in life through family, culture, and personal experiences.

Some people grow up believing:

Money is hard to earn

Rich people are greedy

Saving is impossible

Debt is normal

Others believe:

Money is a tool

Wealth can be built slowly

Financial skills can be learned

Discipline creates freedom

Neither mindset is accidental—but one leads to better outcomes.

Fixed vs Growth Money Mindset

A fixed money mindset believes financial situations cannot change.

A growth money mindset believes skills, habits, and discipline can improve financial outcomes.

Changing your money mindset starts with recognizing which one you currently have.

—

2. Stop Thinking About Money as an Emotional Tool

Many financial problems come from emotional spending rather than logical decisions. People often use money to cope with stress, boredom, or social pressure.

Common emotional money habits include:

Shopping to feel better

Spending to impress others

Avoiding budgets due to fear

Ignoring financial reality

Changing your mindset means separating emotions from money decisions. Money should serve your goals—not your temporary feelings.

Simple Habit:

Before any purchase, ask:

> “Does this move me closer to or further from my long-term goals?”

This single question can save thousands over time.

—

3. Learn to Delay Gratification (The Real Wealth Skill)

Wealth is rarely built overnight. It’s built through delayed gratification—the ability to say no now to say yes later.

People with strong money mindsets understand:

Saving beats impulse spending

Long-term comfort beats short-term pleasure

Financial peace beats temporary excitement

This doesn’t mean never enjoying money. It means choosing enjoyment intentionally.

Practical Tip:

Create a 24-hour rule for non-essential purchases.

If you still want it tomorrow, buy it. Most impulse desires disappear.

—

4. Shift From “How Much I Earn” to “How I Use It”

Income matters—but how you manage money matters more.

Many high earners live paycheck to paycheck because their spending rises with income. People with healthy money mindsets focus on:

Savings rate

Expense control

Investment consistency

Key Insight:

It’s not about how much you make—it’s about how much you keep and grow.

Even small incomes can build wealth with disciplined habits.

—

5. Build the Habit of Paying Yourself First

One of the most powerful mindset shifts is treating savings as a non-negotiable expense.

Instead of saving what’s left after spending, reverse the process:

1. Save first

2. Spend what remains

This habit trains your brain to prioritize future security over present comfort.

Simple System:

Automate savings immediately after income arrives

Start small (5–10%)

Increase gradually

Consistency matters more than amount.

—

6. Understand the Difference Between Assets and Liabilities

A strong money mindset recognizes the difference between:

Assets: things that put money in your pocket

Liabilities: things that take money out

Many people mistake expensive items for wealth when they actually increase financial pressure.

Wealth-focused thinkers ask:

> “Will this grow my future income or drain it?”

This shift alone can completely change long-term outcomes.

—

7. Stop Comparing Your Finances to Others

Comparison is one of the biggest mindset killers. Social media creates unrealistic financial expectations and pressure.

You never see:

Their debt

Their stress

Their financial mistakes

Comparing your financial journey to others leads to poor decisions.

Better Focus:

Compare yourself only to your past self:

Are you saving more?

Are you learning more?

Are you improving gradually?

Progress beats perfection.

—

8. Replace Financial Fear With Financial Education

Fear often comes from lack of understanding. People avoid money topics because they feel overwhelmed or intimidated.

A growth money mindset embraces learning:

Basic budgeting

Simple investing principles

Debt management

Financial planning

You don’t need to become an expert—just informed enough to make better choices.

Small Step:

Commit to learning one money concept per week. Over time, confidence replaces fear.

—

9. Learn to See Money as a Tool, Not a Goal

Money alone doesn’t create happiness—but it provides options, security, and freedom.

Healthy money thinkers use money to:

Reduce stress

Gain time flexibility

Support loved ones

Build meaningful lives

When money becomes a tool instead of an obsession, decisions become clearer and healthier.

—

10. Create Long-Term Financial Goals (Not Just Short-Term Wants)

Without goals, money disappears. With goals, money becomes purposeful.

Strong financial goals are:

Specific

Measurable

Realistic

Time-based

Examples:

Emergency fund within 12 months

Debt-free by a certain year

Investment portfolio by age goal

Goals give direction to every financial choice.

—

11. Accept That Mistakes Are Part of the Process

No one builds wealth perfectly. Mistakes are unavoidable—and necessary.

A strong money mindset:

Learns from mistakes

Adjusts behavior

Avoids shame

Keeps moving forward

Financial growth is not linear. Progress matters more than perfection.

—

12. Build Consistency Over Motivation

Motivation fades. Systems last.

Wealth is built through boring, repeated actions:

Saving monthly

Investing regularly

Tracking spending

Reviewing goals

Consistency beats intensity every time.

—

Conclusion: Changing Your Money Mindset Changes Your Life

Changing your money mindset doesn’t require a massive income, extreme discipline, or financial genius. It requires awareness, patience, and consistent habits.

When you change how you think about money, everything else follows:

Better decisions

Less stress

More control

Long-term security

Wealth is not about luck—it’s about mindset shaped by daily choices.

Start small. Stay consistent. And remember: the most powerful investment you can make is in how you think about money.

—

How to Protect Your Money and Build Financial Stability

Inflation-ku waa heerka uu qiimaha badeecaduhu iyo adeegyada ay kordhaan. Waxaa la filayaa in 2026-2028 uu socdo cadaadis dhaqaale oo xooggan—qiime maciishad sareeya, mushahar aan si dhaqso ah u kicin, iyo sicir barar joogto ah oo saamayn ku yeesha dakhligii caadiga ahaa.

Si kastaba ha ahaatee, qof walba wuu ka badbaadi karaa haddii uu si caqli leh ula tacaalo dhaqaalihiisa. Haddaba aan ka bilowno:

—

—

1. Track Your Daily Expenses and Cut Unnecessary Spending

✔ Why This Works

Marka sicir barar jiro, lacagtu waxay lumisaa qiimaheedii, sidaas darteed waa inaad maamushaa wax kasta oo baxaya.

✔ What To Do

Samee daily spending sheet

Adeegso apps sida

Wallet

Money Manager

Excel Tracker

“WAA IN AAD XAMARSIISO HAL SENT KALE”

✔ What To Cut

❌ Sugars & Soft drinks

❌ Outdoor eating

❌ Luxury accessories

❌ Frequent delivery charges

✔ Where to Move That Money

✔ Emergency fund

✔ Investment account

✔ Debt payments

—

—

2. Build a 6–12 Month Emergency Fund Immediately

✔ Why This Is Critical

Inflation → Prices up → Salary same → Debt risk

Emergency fund waa lifeline-kaaga.

✔ Where to Save It

✔ Bank account with zero withdrawal charges

✔ Digital wallet

✔ Short-term savings account

✔ How Much Should You Save?

> Monthly expenses × 6

Monthly expenses × 12 (best)

✔ What Makes It Powerful

Avoid borrowing when unexpected costs come

Protects mental well-being

Provides flexibility when income delays occur

—

—

3. Pay Down High-Interest Debt Quickly

✔ Why Inflation + Debt Is Dangerous

Debt interest always grows faster than savings.

Inflation increases cost → bank charges stay same → burden doubles

✔ What Debts To Clear First

Loans above interest of 8%

Credit card installments

Consumer loans

Debt Strategy:

⭐ Snowball Method

Pay smallest → psychologically motivating

⭐ Avalanche Method

Pay highest interest → mathematically best

—

—

4. Invest in Long-Term Assets Not Short-Term Consumption

Inflation destroys cash, but it increases the value of assets.

Assets that grow historically

✔ Stocks

✔ Index Funds

✔ Precious Metals

✔ Real Estate

Assets that lose value

❌ Expensive electronics

❌ Fast-depreciating vehicles

❌ Fashion goods

❌ Frequent paid entertainment

—

—

5. Learn Digital Skills That Increase Your Earning Power

Calaamadaha suuqa maanta waxa ka mid ah:

Remote work

AI-driven marketplaces

Rising demand for digital knowledge

Skills you can learn in 30–120 days

Content writing

Graphic design

WordPress

Social media management

Freelance bookkeeping

AI-prompting specialist

Inflation lama kaado → Income is increased.

—

—

6. Convert a Portion of Your Cash to Stable Assets

US Markets showed:

Cash → loses purchasing value

Gold → grows in crisis

Index funds → stable over time

Example Strategy

20% Emergency & expense

40% Medium-term savings

40% Long-term investment

—

—

7. Negotiate Every Major Monthly Bill

Inflation-ku asaga ayaa qiimaha kor u qaadaya, adna waa inaad ku dagaalantaa dhanka khasaaraha.

What to negotiate

✔ Rent

✔ Work transport

✔ Mobile packages

✔ Health coverage

✔ School fees

Techniques

Pay 3–6 months upfront → get discount

Ask student, loyalty, seasonal or referral discount

—

—

8. Stop Emotional and Impulsive Purchases

Inflation waa imtixaanka adkeysiga.

What emotional buyers say:

> “I will buy it now because price will increase tomorrow.”

What financially strong person says:

> “Do I need it today?”

Emotional spending triggers

⚠ Boredom

⚠ Comparison with others

⚠ Social media lifestyle

Fix them

✔ Delay buying 48 hours

✔ Compare prices

✔ Ask “Does this improve my life?”

—

—

9. Build Multiple Streams of Income

Suuqa maanta waxaa caan ka ah:

✔ Side hustle

✔ Subscription monetization

✔ Online freelance

✔ Small reselling

Examples

Offer translation services

Sell digital templates

Affiliate marketing

Online tutoring

One strong rule:

> If one income stops, the second one protects you.

—

—

10. Stay Educated & Follow Financial Trends

2026-2030 waa xilli go’aan qaadasho.

Topics to learn

Inflation cycles

Global interest rate changes

New digital investment products

What Countries Have Highest Impact

USA Federal rate change

EU inflation reforms

When you stay informed → money decisions are accurate.

—

—

—

⭐ Conclusion

Inflation is not your enemy—lack of plan is!

If you track your money, reduce unnecessary spending, invest wisely, and build alternative income sources, inflation becomes simply a change in economic condition—not a disaster.

The strongest foundation in 2026 will belong to the person who:

✔ Spends intentionally

✔ Saves aggressively

✔ Develops marketable skills

✔ Invests for the future

> “Those who prepare early enjoy stability later.”

Managing and growing money has become easier than ever before. You no longer need to walk into a bank, find an investor, or understand complicated charts before investing. Today, everything happens from your phone—within minutes.

However, with thousands of platforms online, the challenge now is not how to invest but where to invest safely and get long-term benefits.

In this guide, we will go step-by-step through how a beginner can choose the right investment platform in 2025. Whether your goal is to buy stocks, save for the future, invest small amounts, or build long-term wealth, this article simplifies it all.

—

—

Why Choosing the Right Platform Matters

Before putting your money anywhere, you must understand the impact of choosing the right platform:

✔ Your money’s safety depends on the platform

Not every website is regulated, and some disappear with user funds.

✔ Your profits depend on fees

A platform may charge hidden withdrawal fees, high commissions, or conversion fees.

✔ Your ability to grow depends on available tools

Some platforms help you:

track stocks,

automate investments,

educate you,

and offer fractional shares.

So choosing correctly can either build wealth or cause losses.

—

—

What Makes an Investment Platform Good in 2025?

When selecting an investment app or brokerage, look for:

—

1. Regulation & Licensing (Most Important Factor)

This determines whether your money is legally protected.

Look for platforms regulated by:

FCA (UK)

CySEC (Europe)

SEC (USA)

ASIC (Australia)

Why this matters:

If something happens to the platform, regulators ensure you receive compensation and proper reporting.

—

2. Ability to Invest With Small Money

Beginners rarely start large.

A good platform should allow: ✔ $5–$50 deposits

✔ fractional shares

✔ no penalty for low accounts

Example: Buying Apple stock for $10 (fractional, not full share).

—

3. Low Fees

Watch out for:

deposit charges

withdrawal fees

trading commissions

inactivity fees

Some platforms earn more through fees than through real trading.

—

4. Investment Choices

A strong platform should allow access to: ✔ stocks

✔ ETFs

✔ bonds

✔ cryptocurrencies (optional)

✔ global markets

This helps diversify your risk.

Example:

Apple stock drops → bond investment still earns stable returns.

—

5. Research Tools Included

Good platforms give:

real-time charts

company financial reports

analysis tools

educational sections

This helps beginners make informed decisions—not emotional ones.

—

—

Signs of a Weak or Risky Investment Platform

Avoid platforms that:

❌ Have no regulatory license

❌ Have complicated withdrawal processes

❌ Promise guaranteed profit

❌ Ask for deposits before account verification

❌ Have little or no customer support

❌ Push signals and VIP paid trading groups

If a platform promises:

> “Guaranteed 50% in one week”

That is a scam.

Investment returns always fluctuate.

—

—

Top Investment Categories for Beginners

Before choosing the platform, choose your direction.

—

Category 1: Long-Term Stock Investing

Best for: ✔ Job holders

✔ Students

✔ People building financial freedom

Why?

Stocks historically outperform banks.

Average 10-year return: 7%–12% annually.

Best for: ⏳ Long term (2–10+ years)

—

Category 2: ETFs

ETF stands for “Exchange-Traded Fund”:

instead of buying one company, you buy 100–500 companies at once.

Example: S&P 500 ETF = Investment into top 500 US companies

This protects your money from single company risk.

—

Category 3: Bonds

Low risk

Stable

Government-backed

Return range: 3%–6% yearly

Perfect for emergency savings.

—

Category 4: Real-Time Trading (Active Trading)

Most beginners want trading because: “money moves fast”.

But note:

> 80% of beginners lose money in trading

Trading is skill-based, emotional, and risky.

Only recommended after learning.

—

—

Step-by-Step Guide: How to Choose an Investment Platform Today

—

Step 1: Confirm Regulation

Visit their website footer

Check license details

Search license on regulator website

If you cannot find it—skip that platform.

—

Step 2: Check Deposit and Withdrawal Options

Look for: ✔ Mobile wallet support

✔ Visa/Mastercard

✔ Bank transfer

✔ Local processing

Withdrawal times should not exceed 48–72 hours.

—

Step 3: Check Fees

Good fees look like:

0% deposit fee

0% withdrawal fee

Low trading commission

If fee structure is hidden → avoid them.

—

Step 4: Check Market Access

A good platform allows investments into: ✔ US markets

✔ European markets

✔ Global ETFs

Why?

More choice = less risk + higher opportunity.

—

Step 5: See If They Support Fractional Investing

Example:

Instead of buying Tesla at $200

You purchase: 👉 $5 worth

This is beginner-friendly.

—

—

How Beginners Can Start With Only $10–$100

Even small money can grow long term:

Example:

Investing $20 every month

10% average yearly return

10 years later = Approx $4,200–$6,000

If you increase contribution → results double.

This is called Dollar-Cost Averaging (DCA).

—

—

Common Mistakes Beginners Make

Avoid these:

—

❌ Investing without research

People follow trends: “Dollar is falling, invest here” “Gold is rising, buy now” “Crypto is exploding”

These emotional choices cause losses.

—

❌ Investing large amount immediately

Start small

Increase gradually

—

❌ Trading before understanding charts

Trading is not luck

It’s strategy.

—

❌ Not diversifying

Example mistake: “Buy only crypto” “Buy only one company”

Diversify = reduce damage.

—

—

How to Build a Simple Beginner Portfolio

Example Starter Portfolio ($100)

Asset Type Amount Reason

ETF (S&P500) $50 Broad exposure

Stock (Apple/Google/Meta) $30 Long-term growth

Bond/Fixed Savings $20 Safety / balance

This structure protects you from heavy loss.

—

What You Should Research Before Buying

Look at: ✔ Company revenue

✔ Future plans

✔ Stability

✔ Market demand

Example:

Apple’s income comes from devices + services

High innovation

Brand loyalty

Low risk

→ Suitable for long term

—

—

The Golden Rule of Smart Investing

> Buy companies and assets you truly understand.

If you don’t understand crypto → avoid it

If a company is unclear → avoid it

If investment feels suspicious → avoid it

Money is safer when decisions are simple.

—

—

Final Conclusion

If you are just starting your investment journey in 2025, take it step-by-step:

✔ Choose regulated platforms

✔ Start with small amounts

✔ Avoid hype and shortcuts

✔ Diversify your portfolio

✔ Think long-term

You don’t need thousands to start.

You only need consistency, patience, and knowledge.

In 5–10 years, these small investments can turn into a strong financial foundation—especially if you follow the rules mentioned in this guide.

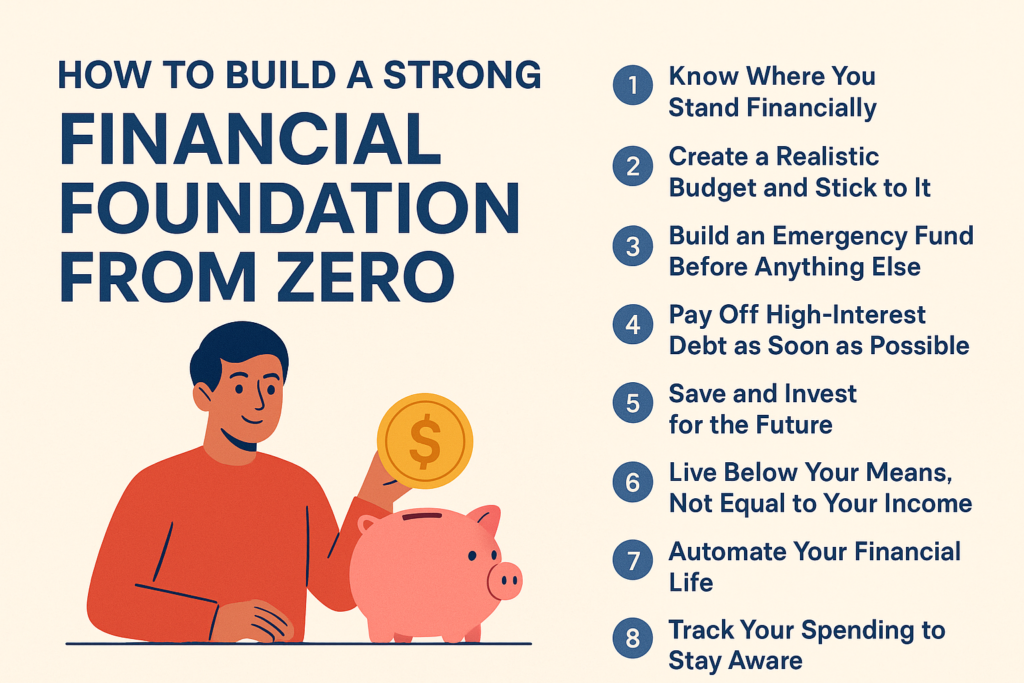

Building a strong financial foundation does not require starting with wealth—it requires starting with clarity, discipline, and consistent action. The eight steps we covered are a complete roadmap for anyone who wants to go from zero to financially stable and eventually financially independent.

You begin by understanding where you stand today, you create realistic financial goals, and then you arrange your spending so that every dollar has a purpose. From there, the journey becomes about protecting yourself, avoiding financial traps, and building systems that work automatically on your behalf. Each tip supports the next, creating a structure that gets stronger with time.

Here is what matters most:

Read:

https://dhilaalo.com/how-to-build-a-strong-financial-foundation-from-zero/

—

✔ Tip #1: Know Where You Stand Financially

You cannot change what you don’t measure. Awareness is your first source of power.

Read:

https://dhilaalo.com/know-where-you-stand-financially/

—

✔ Tip #2: Create a Realistic Budget and Stick to It

A written budget guides your spending instead of letting habits control you.

Read:

https://dhilaalo.com/how-to-create-a-realistic-monthly-budget/

—

✔ Tip #3: Build an Emergency Fund Before Anything Else

This protects you from financial shocks and helps you stay debt-free.

Read:

https://dhilaalo.com/build-an-emergency-fund-before-anything-else/

—

✔ Tip #4: Pay Off High-Interest Debt as Soon as Possible

Debt slows you down, drains your income, and limits financial freedom.

Read:

https://dhilaalo.com/pay-off-high-interest-debt-as-soon-as-possible/

—

✔ Tip #5: Live Below Your Means—No Matter Your Income

Long-term financial strength comes from spending less than you earn.

Read:

https://dhilaalo.com/track-your-spending-to-stay-in-control-of-your-money/

—

✔ Tip #6: Diversify Your Income Streams

One source of income is risky—extra streams increase stability and opportunity.

—

✔ Tip #7: Automate Your Finances

Automation forces consistency even when motivation is low.

Read:

https://dhilaalo.com/automate-your-finances-to-stay-consistent/

—

✔ Tip #8: Track Your Spending to Stay Aware

Awareness keeps you in control and prevents financial slip-ups.

Read:

https://dhilaalo.com/track-your-spending-to-improve-your-financial-awareness/

—

Why This System Works

Every tip above builds on another:

When you know where your money goes → you budget better

When you budget better → you save more

When you save more → you build emergency security

When you are financially secure → you avoid debt

When you avoid debt → your income builds wealth

When wealth grows → you can invest and expand earnings

It’s a cycle of progress.

—

What Happens If You Stick to These Steps?

Within weeks, you will: ✔ See where your money is being wasted

✔ Feel more control at the end of the month

✔ Reduce debt stress

Within months, you will: ✔ Have a safety net

✔ Spend confidently

✔ Save consistently

Within years, you will: ✔ Build real wealth

✔ Experience financial freedom

✔ Afford better opportunities

This isn’t theory—it’s life-changing financial practice.

—

Final Thought

Starting from zero is not a disadvantage.

It is actually clarity.

You have nothing to maintain and everything to build.

Every strong financial journey begins with the same simple choice:

To manage your money before it manages you.

If you follow these eight steps with discipline, your financial foundation will not only be strong, it will be unshakeable—no matter where you started.

—

Simple Tracking = Smarter Decisions + Stronger Financial Control

—

Introduction: Why Tracking Your Spending Matters

Most people don’t realize where their money goes each month. They know they spend “a lot,” but they don’t know exactly how much or on what categories. Tracking your spending gives you the clarity you need to make better financial decisions, reduce waste, and build long-term wealth. It is one of the simplest habits with the biggest impact.

—

What It Means to Track Your Spending

Tracking your spending means recording every expense you make—whether big or small—so you can understand your financial patterns. It helps you see:

How much money goes to essentials

How much is wasted on unnecessary spending

Where you can cut back to save more

How your daily choices affect your monthly financial health

The goal is not to restrict your life, but to gain control.

—

Why Tracking Expenses Is the Foundation of Financial Success

1. It Increases Your Financial Awareness

When you see every dollar you spend, you become more mindful. You stop buying things without thinking.

2. It Helps You Identify Bad Spending Habits

Small purchases add up quickly. Tracking expenses reveals patterns you never noticed.

3. It Allows You to Create a Realistic Budget

You cannot build an effective budget without first knowing your true spending habits.

4. It Helps You Set Achievable Financial Goals

Saving for an emergency fund, paying off debt, or investing becomes easier when you know exactly how much money you can allocate.

5. It Reduces Stress

Financial stress usually comes from uncertainty. When everything is tracked and clear, you gain peace of mind.

—

How to Start Tracking Your Spending

1. Choose a Tracking Method

Pick one that fits your lifestyle:

Finance apps (Mint, PocketGuard, YNAB, etc.)

A simple Excel or Google Sheet

A notebook you update every day

Bank statements + manual categorization

2. Track Every Expense Daily

Write down or record everything:

Food

Transport

Bills

Entertainment

Savings

Subscriptions

Consistency is more important than perfection.

3. Categorize Your Spending

Group your expenses so patterns become easy to see:

Essentials (rent, groceries, utilities)

Non-essentials (eating out, clothing, hobbies)

Financial growth (savings, investments, debt)

4. Review Weekly or Monthly

Ask yourself:

Where did most of my money go?

What spending category surprised me?

What can I reduce next month?

Did I move closer to my financial goals?

—

Tips to Stay Consistent

Use apps that track automatically

Set reminders on your phone

Review your expenses at the same time each day

Keep the process simple—don’t overcomplicate

Reward yourself when you meet monthly goals

—

How Tracking Spending Helps With Long-Term Wealth

When you track your expenses over months and years, you begin to understand your financial behavior deeply. This leads to:

Higher savings rate

Faster debt payoff

Easier emergency fund building

Better investment opportunities

Increased financial confidence

Small daily habits create big long-term results.

—

Conclusion

Tracking your spending is not difficult, but it is one of the most powerful financial habits you can build. It gives you clarity, control, and confidence—three essential ingredients for financial freedom. Start today with whatever method feels simplest, and in just a few weeks, you’ll see a major shift in how you spend, save, and manage your money.

—

Introduction

Many people who start their personal finance journey focus on saving money, investing early, or increasing their income. All these things are great—but none of them matter if you’re still trapped under high-interest debt. Debt with a high interest rate acts like a silent financial drain that slowly eats away your savings, future investments, and monthly budget.

If you don’t prioritize paying it off, high-interest debt keeps growing on its own. It makes it nearly impossible to build wealth because the money you should be saving or investing ends up going toward interest instead of your actual balance.

Paying off high-interest debt isn’t just a financial step—it’s the foundation that makes saving, investing, and long-term planning possible.

—

Section 1: What Counts as High-Interest Debt?

High-interest debt is any debt that charges 10%–15% interest or more. But typically, financial experts consider anything above 18% as high-risk debt that must be paid off immediately.

Common examples include:

Credit card debt (15%–35%)

Online loans or micro-loans (20%–200% APR)

Buy Now Pay Later loans with hidden fees

Bank overdraft penalties and interest

Store financing (electronics, furniture, appliances)

Emergency loans from loan apps

The biggest problem with this type of debt is not the amount you borrowed—

it’s the compound interest that grows month after month.

—

Section 2: Why High-Interest Debt Is a Financial Emergency

1. It destroys your ability to save

If you pay $70–$100 a month in interest, that’s $840–$1,200 a year completely wasted.

This money could have gone into:

Savings

Investments

Emergency fund

Education or business

Interest is money you get nothing for.

—

2. It keeps you living paycheck-to-paycheck

The more debt payments you have, the tighter your budget becomes.

This makes it harder to build any financial stability or flexibility.

—

3. It lowers your credit score

High debt utilization and late payments cause:

Lower credit score

Higher loan interest in the future

Reduced approval chances for rentals or financing

Debt affects more than your wallet—it affects your opportunities.

—

4. It blocks your ability to invest

There is no point making a 10% profit from investments when you are losing 25% in debt interest.

You are always behind.

—

5. It increases stress and mental pressure

High-interest debt is one of the biggest causes of:

Anxiety

Sleepless nights

Relationship conflict

Financial insecurity

Paying it off brings peace of mind as much as it brings financial freedom.

—

Section 3: Step-by-Step Plan to Pay Off High-Interest Debt

Step 1: Get a full picture of your debt

Write down:

Total debt amount

Interest rate (%)

Minimum monthly payment

Due dates

Lender name

You cannot fix what you do not understand.

—

Step 2: Prioritize your debts

Sort your debts into three levels:

High-interest (top priority)

Medium-interest

Low-interest

Anything above 15% should be dealt with immediately.

—

Step 3: Choose Your Payment Strategy

Strategy A: Avalanche Method (Fastest & most efficient)

Pay off the highest interest debt first.

Benefits:

Saves more money

Clears debt faster

—

Strategy B: Snowball Method (Motivation booster)

Pay off the smallest balance first to build momentum.

Benefits:

Quick emotional wins

Keeps you motivated

—

Step 4: Reduce unnecessary expenses

To accelerate payments:

Cut small daily expenses

Avoid impulse buying

Reduce deliveries and subscriptions

Track your spending

Identify wasteful habits

Every dollar saved becomes a weapon against debt.

—

Step 5: Build a simple payment plan

Your monthly flow should look like this:

Income → Essential bills → Debt payments → Savings

A steady, predictable plan beats random payments.

—

Section 4: 10 Proven Ways to Pay Off Debt Faster

1. Automate your payments

Avoid late fees and reduce risk of missed payments.

2. Pay more than the minimum

Even $10–$20 extra per month makes a difference.

3. Make bi-weekly payments

Two smaller payments reduce interest over time.

4. Use side income for debt

Freelancing, online gigs, design, writing—use any extra income for debt reduction.

5. “No-Spend Weeks”

Avoid spending on non-essentials for 7 days straight.

6. Debt consolidation (if available)

One lower-interest loan replacing multiple high-interest ones.

7. Avoid using credit while paying it off

Don’t add more debt.

8. Renegotiate your interest rate

Banks and lenders sometimes:

Lower interest

Waive fees

Offer new payment plans

Just ask.

9. Sell unused items

Turn clutter into cash.

10. Track your progress

Seeing the numbers drop keeps you motivated.

—

Section 5: How Paying Off High-Interest Debt Changes Your Life

1. Immediate financial relief

No more heavy monthly payments draining your income.

2. Higher credit score

Better access to:

Loans

Rentals

Business financing

3. Stress reduction

Less money pressure means better mental health.

4. Faster savings and investment growth

Money that once went to interest now goes to your goals.

5. True long-term freedom

Once debt is gone, you can:

Build wealth

Start a business

Save for big goals

Live without fear

—

Conclusion

Paying off high-interest debt early is one of the smartest financial decisions you will ever make.

It gives you:

More money

More freedom

More confidence

More stability

When you eliminate the debt that’s secretly holding you back, you open the door to a secure, independent, and powerful financial future.

(Long, SEO-optimized, Ads-friendly & Beginner-friendly)

Automation is one of the most underrated yet powerful strategies in personal finance. Many people struggle with consistency — saving one month, forgetting the next; paying bills late; or losing track of debt payments. Automating your finances eliminates these problems by making your money work without requiring daily willpower.

Below is a deeply detailed breakdown designed for SEO optimization, readability, and maximum value.

—

What Does “Automating Your Finances” Really Mean?

Automating your finances means using digital tools, bank features, and budgeting apps to allow your money to automatically move to the right places without you manually doing it each month.

This includes automating:

✔ Savings transfers

✔ Emergency fund contributions

✔ Investment deposits

✔ Debt payments

✔ Bill payments

✔ Budget tracking

✔ Expense notifications

Instead of you managing money, the system manages it for you.

—

Why

Automation Is a Game-Changer (Backed by Psychology & Data)

One of the biggest obstacles for people is inconsistency. Even financially smart people fail to save or pay bills on time because life gets busy.

Automation solves these psychological problems:

Removes the need for daily discipline

When money moves automatically, you don’t need motivation or memory.

Prevents emotional spending

If your money goes to savings before you touch it, you can’t spend it carelessly.

Ensures consistent progress

Even when you’re busy, sick, traveling, or stressed, your financial system keeps working.

Reduces stress and decision fatigue

Fewer decisions = fewer mistakes.

Builds habits effortlessly

Repeating automated actions creates long-term stability.

—

How to Set Up Full Financial Automation (Step-by-Step Guide)

This section is designed for SEO and actionable advice.

—

Step 1: Choose a Primary Bank for Incoming Income

Make sure salary or business earnings land in one main account. This is the “root” of your financial tree.

SEO Keywords: primary account, salary account, personal finance setup, banking automation.

—

Step 2: Set Automatic Transfers for Savings

Automate a percentage of income (even 5–10%) to a dedicated savings account.

Set this transfer to happen:

the same day your income arrives

every month without fail

This protects your money before you start spending.

—

Step 3: Automate Your Emergency Fund Contributions

Your emergency fund should grow every month without manual effort.

Example:

Every 1st date → $10 / $20 / $50 to Emergency Account

Continue until you hit 3–6 months of expenses

This creates financial protection instantly.

—

Step 4: Automate Debt Payments

High-interest debt becomes cheaper and easier when paid automatically.

Automation helps you:

avoid late fees

reduce interest accumulation

build a perfect payment history

Set automatic payments for: ✔ Credit cards

✔ Loans

✔ Financing plans

—

Step 5: Automate Investments

If you invest manually, you’ll skip months.

Automated investing ensures long-term growth.

Examples:

Automatic weekly crypto buys

Automatic stock purchases

Monthly index fund deposits

Automated micro-investing apps

Even $5–$20 regularly compounds hugely over years.

—

Step 6: Set Up Auto-Bill Pay

Automate payments for: ✔ Internet

✔ Phone

✔ Subscriptions

✔ Rent (if your bank supports it)

✔ Insurance

✔ Utilities

This protects your credit and financial reputation.

—

Step 7: Use Budgeting Apps with Auto-Tracking

Apps like:

YNAB

PocketGuard

Mint

Spendee

GoodBudget

These sync your bank transactions automatically and categorize spending for you.

This gives you full visibility without manual work.

—

Benefits of Full Financial Automation

This section is written SEO-style with keyword inclusion.

1. You save more without trying

People who automate savings save 2x to 4x more than those who don’t.

2. You become debt-free faster

Automatic payments shorten debt payoff time.

3. You reduce financial stress

You always know bills are paid and savings are growing.

4. You avoid late fees

Automation protects your credit score.

5. You build long-term wealth effortlessly

Your money grows while you sleep.

—

Common Mistakes to Avoid When Automating Finances

To make the post deeper and more SEO-friendly.

Automating without checking balances

Not updating automation when income changes

Too many small automations that become confusing

Forgetting subscription renewals

Ignoring account alerts

—

Pro Tips to Make Financial Automation Even More Powerful

Use a “Two-Account System”

Account 1 → Salary

Account 2 → Spending

Everything else (savings, investments, bills) is automated before money reaches your hands.

Add Alerts

Set notifications for:

low balance

large purchases

deposit confirmation

failed automation

Review automation every 3 months

This ensures your system stays aligned with your goals.

—

Conclusion: Automation = Financial Freedom

Automating your finances is like hiring a personal financial assistant who works 24/7.

It keeps you consistent, protects your money, prevents stress, and helps you build wealth automatically.

Even if you start small, automation creates long-term transformation.

One of the most powerful habits you can build on your financial journey is tracking your spending consistently. Most people don’t realize where their money goes until they start monitoring it — and once they do, everything becomes clearer: the leaks, the unnecessary expenses, and the habits that slow down financial progress.

Tracking your spending is not about restricting your life.

It’s about understanding your money, recognizing patterns, and making smarter decisions. When you know exactly where every dollar is going, you gain the confidence and clarity to plan your future wisely.

Why Tracking Your Spending Matters

Here’s what happens the moment you start tracking:

You quickly identify where you waste money without realizing it.

You become more intentional with every purchase.

Your savings increase naturally.

You reduce overspending and impulse buying.

You gain full control over your financial life.

Simply put: You can’t fix what you don’t measure.

How to Track Your Spending Effectively

You don’t need complicated systems. These simple methods work extremely well:

1. Use a Budgeting App

Apps like PocketGuard, Mint, Goodbudget, or any local mobile banking tracker can automatically categorize your spending. You just check in weekly.

2. Use a Simple Google Sheet or Notebook

Some people prefer manual tracking. Writing things down increases awareness and discipline.

3. Review Your Daily or Weekly Spending

Set 5–10 minutes every week to check your expenses.

This habit alone can change your entire financial lifestyle.

4. Create Spending Categories

Break expenses into simple groups:

Essentials: Rent, food, bills, transport

Important: Savings, investments, emergency fund

Optional: Restaurants, entertainment, clothing

Waste: Things you regret buying

Once you see your “waste” clearly, it becomes easier to reduce it.

What You Gain from Tracking Spending

More savings without stress

Better budgeting

Financial peace of mind

Faster progress toward your goals

A realistic picture of your spending behavior

Tracking spending is a habit that pays you back every single day.