Building wealth is not about one big decision — it’s about small actions repeated consistently. One of the most effective ways to make sure you stay on track is to automate your savings. When your savings happen without you manually transferring money, you remove temptation, reduce stress, and guarantee progress toward your financial goals.

Automation ensures that every time you earn money, part of it moves directly into your savings or investment accounts. This makes saving effortless, consistent, and predictable — even during busy or stressful periods.

Why Automating Your Savings Works

You save before you spend, preventing overspending.

It builds a habit without requiring daily discipline.

You avoid forgetting to save during months when expenses feel heavy.

Your wealth grows steadily, even with small contributions.

It reduces financial stress by giving your money a clear plan.

How to Automate Your Savings Effectively

1. Choose Your Savings Goal

It could be an emergency fund, travel savings, a business fund, or long-term investing.

2. Decide the Percentage You Can Save Automatically

Even 5%–10% of your income makes a huge difference over time.

3. Set Up Automatic Transfers

Most banks allow you to schedule automatic weekly or monthly transfers.

4. Use Budgeting Apps or Digital Banks

Many apps automatically separate your money into “saving buckets” the moment you get paid.

5. Increase the Amount Over Time

Whenever your income grows, adjust your automated savings upward.

The Power of “Set It and Forget It”

Automating your savings removes emotional decisions. You don’t have to think about discipline, motivation, or timing — the system handles everything. Over several months, you’ll start to see visible progress, which boosts confidence and keeps you focused.

Long-Term Benefits

More financial stability

Less stress during emergencies

Faster progress toward major goals

Stronger credit and financial profile

A foundation for long-term investing

—

A Step-by-Step Guide to Protecting Your Financial Future

An emergency fund is one of the most important pillars of strong personal finance. No matter how stable your income seems, life can always throw unexpected challenges—medical emergencies, job loss, car repairs, family needs, or sudden bills.

Having an emergency fund ensures that you stay safe, confident, and financially protected during difficult times.

In this guide, you will learn what an emergency fund is, why you need it, and how to build it even if your income is small.

—

What Is an Emergency Fund?

An emergency fund is a separate amount of money saved to cover unexpected expenses. This money is not for shopping, travel, entertainment, or normal bills.

It is ONLY for real emergencies.

Examples of true emergencies:

Medical treatments

Job loss

Urgent home or car repairs

Unexpected family needs

Sudden income interruption

Having money ready for these moments protects you from taking loans, falling into debt, or selling your belongings.

—

Why You Need an Emergency Fund

Building an emergency fund gives you:

1. Financial Security

You won’t panic when an unexpected expense appears.

2. Peace of Mind

Knowing that you have savings reduces stress and improves decision-making.

3. Protection From Debt

When emergencies happen, many people borrow money at high interest. An emergency fund saves you from that trap.

4. Freedom to Make Better Choices

You can change jobs, start a side hustle, or move houses without fear of going broke.

—

How Much Should You Save?

Most financial experts recommend:

➤ Save 3–6 months of your monthly expenses

Example:

If you spend $200 per month, aim for $600–$1,200 in your emergency fund.

But don’t worry if that sounds too big. You can start small.

If your income is low, start with this simple rule:

✔ Save $1 a day

✔ Save $5–$10 per week

✔ Save 10% of any extra income

Small steps build a big result over time.

—

Where Should You Keep Your Emergency Fund?

Keep your emergency fund in a safe, separate place, such as:

A savings account

Mobile money savings feature (if available in your country)

A secure bank account

A digital wallet with savings options

Do NOT mix it with your daily spending money.

—

How to Start Building Your Emergency Fund

Follow these steps:

1. Calculate Your Monthly Needs

Include:

Food

Transport

Rent

Utilities

School fees

Medical expenses

This helps you know the exact target.

2. Cut Small Unnecessary Expenses

Even small things add up:

Eating out too often

Extra subscriptions

Unplanned shopping

Redirect that money to your emergency fund.

3. Automate Your Savings

If possible, set automatic transfers weekly or monthly.

This is the easiest way to stay consistent.

4. Increase Your Savings When Income Grows

Any extra income (freelancing, business, bonuses) → put part of it aside.

5. Never Use the Fund Unless It’s Truly an Emergency

This maintains discipline and keeps your fund growing.

—

How Long Does It Take to Build an Emergency Fund?

It depends on your income, discipline, and lifestyle.

Some people build their fund in 3 months, others in 1 year.

The goal is consistency—not speed.

Even saving $20 per month is better than saving nothing.

—

Common Mistakes to Avoid

Using the fund for normal expenses

Saving without a target

Keeping the money where you can easily spend it

Not reviewing your progress monthly

Avoiding these mistakes will help your emergency fund grow faster.

—

Final Thoughts

An emergency fund is not just money—it is security, confidence, and financial freedom.

Even if you earn a small income, starting with tiny contributions can transform your financial life over time.

—

—

Introduction

Life is unpredictable. Emergencies don’t ask permission. They don’t follow your schedule. They don’t wait for your salary date.

A sudden medical bill, a family crisis, a broken phone, a job loss, or even a simple repair can push a person into debt within hours.

This is why every financial expert agrees on one rule:

> The first step to financial stability is building an emergency fund.

Not investing.

Not budgeting.

Not saving for goals.

Your emergency fund is Step Number One.

In this comprehensive guide, we explore everything you need:

What an emergency fund really is

Why it matters

How much to save

How to start even with low income

Where to keep the money

How to grow the fund

How to protect it

Common mistakes people make

Step-by-step plan for your first 100 days

This article will be your ultimate guide — long, practical, and beginner-friendly.

—

1. What Exactly Is an Emergency Fund?

An emergency fund is a dedicated savings pool meant only for unexpected, urgent situations.

It is not for wants, vacations, new clothes, impulse shopping, or entertainment.

It is specifically meant for:

Medical emergencies

Job loss or income interruption

Family emergencies

Urgent repairs (home or phone)

Essential travel

Emergency bills

Unplanned financial shocks

Think of it as your personal financial shield.

—

2. Why an Emergency Fund Matters More Than Anything Else

Most people underestimate emergencies until they happen. But emergencies are not rare—they are guaranteed.

Here’s why an emergency fund is life-changing:

✔ 1. It protects you from debt

Without savings, the first place you run to is:

Loans

Credit

Borrowing from friends

High-interest lenders

One emergency can trap you in debt for years.

✔ 2. It reduces stress and fear

Money problems destroy peace of mind. But when you have an emergency fund, you feel calm — even when life becomes chaotic.

✔ 3. It gives you financial confidence

You make smarter decisions when you’re not worried constantly.

✔ 4. It prevents paycheck-to-paycheck living

Many people survive by hoping “nothing goes wrong.”

Emergency funds break that cycle.

✔ 5. It helps you focus on long-term goals

When emergencies are covered, you can focus on:

Saving

Investing

Starting a business

Improving your life

—

3. How Much Should You Save? (Beginner, Intermediate, Expert Levels)

Level 1: Starter Emergency Fund (Beginners)

Save $50 – $200 first.

This is your seed.

Small, but powerful.

Level 2: Basic Emergency Fund (Stable Stage)

Save 1 month of living expenses.

This covers rent, food, transport, essentials.

Level 3: Strong Emergency Fund (Experts)

Save 3–6 months of living expenses.

Most financial experts recommend this amount.

Level 4: Maximum Security Fund

Save 12 months of living expenses if:

You have unstable income

You’re self-employed

You live in an expensive city

You support many people

—

4. How to Calculate Your Emergency Fund

Write down your real monthly expenses:

Category Amount

Rent / Housing X

Food X

Transport X

Utilities X

Medical X

Communication (data/airtime) X

Family support X

Other essentials X

Add all of them.

Multiply by 3 or 6.

This is your goal.

—

5. Where Should You Keep Your Emergency Fund?

The money must be:

Accessible

Safe

Separated from your main money

Not easy to withdraw impulsively

Best places to keep it:

1. Dedicated savings account

2. Mobile savings wallet (with lock feature)

3. Bank digital savings plan

4. High-yield savings accounts (if available in your country)

❌ Never keep your emergency fund in:

Cash at home (unsafe)

Investment accounts (prices can drop)

Business capital

Crypto (too volatile)

Normal spending account (too tempting)

—

6. How to Build an Emergency Fund Even With Low Income

People with small incomes assume they can’t save.

That’s wrong.

Here’s how to start even with very little money:

✔ 1. Start extremely small

Save $1, $2, or $5

Small savings accumulate faster than you think.

✔ 2. Use automation

Set your bank to auto-transfer weekly.

✔ 3. Save unexpected money

Bonuses

Gifts

Side job income

Business profits

Refunds

✔ 4. Cut one unnecessary expense

One meal

One soda

One coffee

One subscription

Redirect it to your fund.

✔ 5. Sell unused items

Old clothes

Old phones

Accessories

Books

Shoes

Small items

Turn them into savings.

—

7. The Psychology of Saving

Money habits come from:

Discipline

Awareness

Emotional control

Saving is 80% mindset, 20% income.

When you commit mentally, your bank account follows.

—

8. Signs You Need an Emergency Fund Immediately

You panic when you have bills

You borrow often

You have no backup income

You support your family

You live paycheck to paycheck

One emergency would destroy your finances

If any of these apply,

your emergency fund is a priority starting today.

—

9. Common Mistakes People Make

❌ Using the fund for non-emergencies

❌ Keeping money where it’s too easy to withdraw

❌ Not replacing money after using it

❌ Believing income is too small to save

❌ Waiting for “the right time”

❌ Mixing emergency funds with investments

—

10. How to Rebuild Your Emergency Fund After Using It

If you use the fund, that’s okay.

That’s why it exists.

Here’s how to rebuild it:

✔ Step 1: Replace money gradually

✔ Step 2: Pause unnecessary expenses

✔ Step 3: Add extra money from side jobs

✔ Step 4: Track your progress weekly

—

11. 100-Day Emergency Fund Challenge

This plan makes saving simple.

Day 1–30

Save small ($1–$3 per day)

Day 31–60

Save medium ($3–$5 per day)

Day 61–100

Save bigger ($5–$7 per day)

By Day 100, you’ll have a solid foundation.

—

12. Long-Term Benefits of an Emergency Fund

You sleep better

You feel more confident

You stop borrowing

You build wealth faster

You invest without fear

You avoid financial crises

—

13. Frequently Asked Questions (FAQ)

Q1: What if I have debt? Should I save first?

Yes. Start with a small emergency fund before paying debts aggressively.

Q2: How do I avoid touching the money?

Keep it in a separate, locked account.

Q3: Should I tell family about it?

No, unless you trust them not to misuse your generosity.

—

Conclusion

Your emergency fund is your financial foundation.

Without it, every step becomes risky.

With it, you gain stability, confidence, and long-term security.

Start today, even if the amount is small.

Your future self will thank you.

—

Introduction

Before you can improve your financial life, you must first understand your current financial situation. Most people struggle with money not because they lack income, but because they don’t clearly know where their money goes, how much they owe, or what their true financial position is.

Knowing where you stand financially is the first and most important step toward financial stability and long-term wealth.

In this guide, we break down exactly how to assess your finances and build a clear picture of your money.

—

What Does “Knowing Your Financial Position” Mean?

It means having a complete and accurate understanding of:

How much money you earn

How much you spend

How much you owe (debts)

How much you save

Your financial habits

What risks you face

What goals you want to achieve

Once you know these, you can control your finances instead of letting money control you.

—

1. Calculate Your Total Monthly Income

Start by listing every source of income you have:

Full-time or part-time job

Freelancing or online work

Small businesses

Side hustles

Commissions or bonuses

Money from services (transport, repairs, etc.)

Add all of them to get your total monthly income.

This number is the foundation for every decision you make.

—

2. Track All Your Monthly Expenses

You cannot improve what you do not measure.

List all your spending for the last 30 days.

Split your expenses into two groups:

A. Essential (Needs)

Food

Rent or housing

Transport

Utilities (electricity, water, internet)

School fees

Medical needs

B. Non-essential (Wants)

Eating out

Entertainment

Shopping

Subscriptions

Luxury items

When you separate these categories, you immediately see where your money leaks.

—

3. List All Your Debts and Responsibilities

Many people avoid checking their debts because it feels uncomfortable.

But ignoring debt only makes it worse.

Write down:

Loans

Credit owed to people

Business debts

Unpaid bills

Installments

Then calculate your total debt.

This helps you plan repayments realistically.

—

4. Review Your Savings and Assets

Knowing what you own is as important as knowing what you owe.

Your assets may include:

Savings account

Mobile money balance

Cash reserves

Land or property

Investments

Equipment or tools used for income

Digital assets

This gives you a clear picture of your net worth.

—

5. Compare Your Income vs. Expenses

This step shows your real financial health:

✔ If income > expenses → you are financially positive

You have room to save, invest, and grow.

✔ If expenses > income → you are financially stressed

You may need to reduce spending or increase income.

✔ If they are equal → no growth, no savings

This is called “living paycheck to paycheck.”

—

6. Identify Financial Weaknesses and Risks

These may include:

No emergency fund

Too many small expenses

Uncontrolled debt

Irregular income

No savings plan

Overspending on non-essential items

Knowing your weaknesses helps you fix them fast.

—

7. Set Clear Financial Goals

Once you know your starting point, choose where you want to go:

Build an emergency fund

Pay off debt

Save for a business

Invest for the future

Increase income

Improve credit reputation

Clear goals guide every financial decision you make.

—

Why This Step Is So Important

Knowing where you stand financially:

Helps you stay disciplined

Prevents financial surprises

Makes budgeting easier

Improves decision-making

Builds confidence and control

Shows you exactly what needs improvement

This is the foundation of smart personal finance.

—

—

Introduction

Budgeting helps you take full control of your finances and understand exactly where your money goes each month. It is one of the most important steps for anyone who wants to build a strong and stable financial future.

While many people think budgeting is complicated, it is actually a simple system that can save you a lot of money and prevent financial stress.

—

1. Calculate Your Total Monthly Income

Start by knowing your exact monthly income.

This includes:

Salary

Freelance payments

Business income

Commissions

Side hustle earnings

Your budget can only work if your income is accurate.

—

2. Track All Your Monthly Expenses

Write down every expense you have each month.

Essential Expenses (Needs):

Rent / Housing

Food and groceries

Transportation

Water & electricity

Internet & phone bills

Non-Essential Expenses (Wants):

Entertainment

Unnecessary clothing

Eating out

Shopping

Travel

Tip:

Use apps like Monefy, Notion, or Google Sheets to track spending easily.

—

3. Use the 50/30/20 Budgeting Rule

This is one of the most popular budgeting methods:

50% → Needs (essential living expenses)

30% → Wants (non-essential but enjoyable)

20% → Savings + investments

If your income is low, adjust it to:

60/25/15

70/20/10

The goal is to create a system that fits your real situation.

—

4. Identify and Reduce Wasteful Spending

After listing your expenses, you will notice unnecessary spending that eats your money.

Examples:

Eating out too often

Subscriptions you never use

Expensive transportation

Buying things you don’t need

Cutting these small costs can save a lot of money every month.

—

5. Set Clear Financial Goals

Your budget should support your goals, such as:

Building an emergency fund

Paying off debt

Saving for a house

Investing for the future

Growing your side income

Write down each goal clearly so you stay focused.

—

6. Use Separate Accounts

To manage your money more effectively, divide your accounts:

One account for expenses

Another for savings

Another for investments

This prevents mixing money and reduces impulse spending.

—

7. Review and Adjust Your Budget Every Month

A budget is not something you create once and forget.

Every month:

Check how much you earned

Compare expected vs actual expenses

Adjust overspending areas

Increase savings if you can

Update any financial changes

A flexible budget is a successful budget.

—

Conclusion

A good budget is simple, realistic, and easy to follow.

It helps you reduce unnecessary spending, increase savings, and build a long-term financial foundation that protects you from stress and uncertainty.

Budgeting is a habit — not a one-time activity.

—

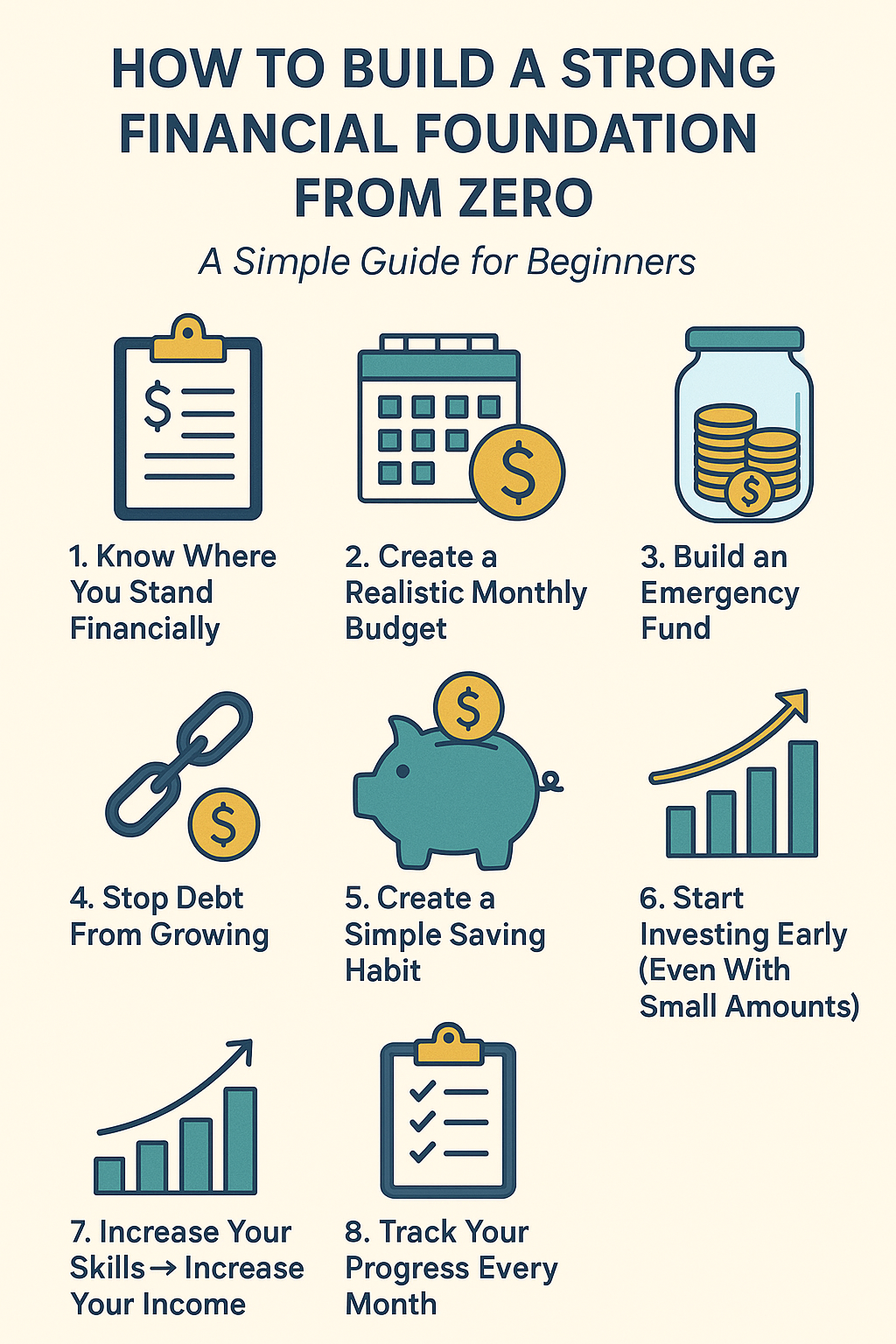

(A Simple Guide for Beginners)

Introduction

Building a strong financial foundation doesn’t require being rich — it starts with simple habits, discipline, and understanding how money works. Whether you’re starting from zero or even from debt, the steps below will help you create a stable financial future.

—

1. Know Where You Stand Financially

Before you improve your money situation, you must understand it.

Ask yourself:

How much do I earn monthly?

How much do I spend?

Do I owe anyone?

Do I save anything?

Just writing these down gives you control.

—

2. Create a Realistic Monthly Budget

A budget is your financial map.

The easiest method for beginners is the 50/30/20 rule:

50% → needs (food, rent, transport)

30% → wants (entertainment, clothes)

20% → savings + investments

If income is small, you can adjust it to 60/25/15 or even 70/20/10.

—

3. Build an Emergency Fund

Life is unpredictable — losing a job, falling sick, or facing sudden expenses.

Start saving little by little until you reach:

1–3 months of expenses (beginners)

3–6 months (ideal)

Even saving $1–5 a day builds a strong cushion over time.

—

4. Stop Debt From Growing

Debt kills your financial progress.

Follow this order:

Stop borrowing completely

Pay high-interest loans first

Avoid “quick money” borrowing apps

Negotiate if possible

You can’t build wealth while debt is growing.

—

5. Create a Simple Saving Habit

Wealth starts with consistent saving, not big numbers.

Try this:

Save 10% of all income automatically

Use a separate account

Never touch savings except for emergencies

This creates discipline and long-term growth.

—

6. Start Investing Early (Even With Small Amounts)

You don’t need big money to invest.

Begin with:

Mobile investment apps

Simple index funds

Gold savings

Low-risk plans (depending on your country)

Small investments grow massively because of compound interest.

—

7. Increase Your Skills → Increase Your Income

The fastest way to grow financially is to grow your skills.

Learn high-income skills

Improve your profession

Take online courses

Start freelancing or side hustles

More income = more saving + more investing.

—

8. Track Your Progress Every Month

Review:

What you earned

What you saved

What you invested

What you overspent

This keeps you accountable and motivated.

—

Conclusion

A strong financial foundation is not about being rich — it’s about having control, planning ahead, and making smart decisions. Start small, stay consistent, and your money will grow with time.

—

Cryptocurrency has transformed global finance over the last decade. From its origins as a niche digital experiment, Bitcoin has become a major financial asset recognized by institutions, corporations, and individual investors.

By 2025, Bitcoin is no longer just an experimental currency—it represents a store of value, an investment vehicle, and a technological innovation.

Investors ask: Is it wise to invest in Bitcoin now? This article explores the truth behind cryptocurrency, the history and mechanics of Bitcoin, market trends, risks, and strategies to consider before investing in 2025.

A cryptocurrency is a digital or virtual currency secured by cryptography, making it nearly impossible to counterfeit. It typically operates on a decentralized network, removing the need for banks or intermediaries.

Beyond currency, cryptocurrencies enable decentralized finance (DeFi), NFT platforms, and programmable blockchain applications. This expands potential uses and investment opportunities.

Bitcoin, launched in 2009 by Satoshi Nakamoto, is the first cryptocurrency. Its innovation lies in solving the double-spending problem without a central authority.

Bitcoin’s scarcity and decentralization make it a potential hedge against inflation and a long-term investment vehicle.

| Year | Milestone | Price & Notes |

|---|---|---|

| 2009 | Bitcoin launched | ~$0, mined by enthusiasts |

| 2010 | First real-world transaction | 10,000 BTC for 2 pizzas |

| 2011 | Bitcoin hits $1 | Early adoption grows |

| 2013 | Price surpasses $1,000 | Media attention increases; bubble forms |

| 2014 | Mt. Gox collapse | ~850,000 BTC lost; price drops |

| 2015 | Ethereum launch | Crypto ecosystem expands beyond currency |

| 2016 | Bitcoin halving | Miner rewards drop; price rises to ~$600–$700 |

| 2017 | Bitcoin peaks ~$20,000 | Speculative retail bubble |

| 2018 | Crypto winter | Price falls to ~$3,200 |

| 2019 | Recovery begins | Price stabilizes ~$7,000–$10,000 |

| 2020 | Second halving & institutional adoption | Price rises ~$28,000; MicroStrategy, Tesla buy BTC |

| 2021 | All-time highs | ~$64,000 in April; volatility remains |

| 2022 | Market correction | Drops to ~$15,000–$20,000 due to macroeconomics and regulations |

| 2023 | Regulatory maturity | Stable ~$25,000–$35,000; adoption grows |

| 2024 | Adoption & tech upgrades | Lightning Network adoption; faster, cheaper transactions |

| 2025 | Future outlook | Volatility remains; institutional support; digital gold potential |

Takeaway: Bitcoin remains the most widely recognized store of value, while altcoins offer diversification and technological innovation.

Bitcoin represents a revolution in finance. By 2025, it is no longer a niche digital currency, but a recognized investment and store of value. For potential investors:

With the right approach, Bitcoin can form a valuable component of a diversified investment strategy, offering potential growth while hedging against traditional financial risks.

As the global economy continues to shift and the cost of living rises, personal finance has become more important than ever in 2025. Whether you’re trying to save money, eliminate debt, or build long-term wealth, smart financial habits can completely change your financial future.

This guide provides the best personal finance tips for 2025, designed to help you save more, spend more wisely, and steadily grow your wealth—no matter your income level.

Let’s dive into the strategies that thousands of high-income and financially successful people use every day.

Budgeting is the foundation of financial success. But in 2025, budgeting is no longer about writing numbers on paper—it’s about tracking your spending in real time.

A good budget = a stronger financial future.

Uncertainty in 2025 remains high—job markets shift, inflation fluctuates, and expenses can rise unexpectedly.

An emergency fund protects you from:

3–6 months of living expenses is ideal.

This money shouldn’t be invested—it should be liquid and accessible.

Automation is one of the most powerful tools in personal finance. In 2025, almost every bank and app allows automatic transfers.

Automation removes emotion from your finances and guarantees consistency.

High-interest debt (especially credit cards) is the biggest wealth killer.

If the interest rate is over 10%, it should be a priority to eliminate it.

Investing is no longer optional in 2025 — it’s the only way to beat inflation and grow real wealth.

Start small, stay consistent, increase gradually.

Even $20–$50 a month grows massively with time thanks to compounding.

Most people focus only on how much they earn, but wealth is built by how much you keep and invest.

Assets – Liabilities

Tracking your net worth:

Apps like Personal Capital or Monarch Money make this easy.

Lifestyle creep happens when your expenses rise as your income rises.

In 2025—with social media pressure and consumer marketing—it’s more dangerous than ever.

Wealthy people expand savings & investments, not lifestyle.

If you spend money, get rewarded for it.

In 2025, smart spending is just as important as saving.

Relying on one income is risky. One job loss can destabilize your entire financial life.

The average millionaire has multiple income streams.

Even if retirement feels far away, planning early gives you exponentially more growth.

The earlier you start → the richer your retirement becomes.

2025 is a year full of financial challenges — but also massive opportunities. By budgeting wisely, saving consistently, investing early, and making smart money decisions, you can build a strong financial foundation that protects your future.

The key is to start now.

Not next month.

Not next year.

Today.

Because money grows with time — and time is the one resource you can’t get back.

Finance is the engine that powers the modern global economy. Whether it’s an individual trying to manage their monthly income, a business seeking growth, or a government controlling inflation, finance sits at the heart of every economic decision.

Despite its importance, most people don’t receive proper financial education — how money works, how to invest, or how to build long-term wealth. This blog post is designed to simplify modern finance and offer a clear, structured understanding of:

If you’re a student, entrepreneur, employee, or anyone looking to strengthen your financial knowledge, this article will give you the clarity and insight you need to navigate the financial world confidently.

Finance refers to the management, creation, and study of money. It includes how money is obtained, how it is spent, how it is invested, and how risks are managed.

Finance operates across three main areas:

Focused on the individual, including:

Deals with how businesses manage:

Government-level financial activities, including:

These three areas work together to create the financial ecosystem that drives economic progress.

Money moves like blood in the body — if circulation stops, the system collapses. Understanding this flow clarifies why economic stability matters.

Government → Infrastructure → Jobs → Household Income → Taxes → New Budget

Breakdowns at any level affect the entire economic cycle.

Inflation refers to the rise in prices of goods and services over time.

Causes of inflation include:

Effects of inflation:

A healthy economy maintains moderate inflation. Too much — or too little — is harmful.

Central banks manage a country’s monetary and financial system. Their key roles include:

When interest rates increase:

When interest rates decrease:

Their main challenge is balancing growth and stability.

Understanding asset classes is essential for smart investing.

Pros: Stable and safe

Cons: Very low returns, often below inflation

Pros: High profit potential

Cons: High volatility and risk

Real assets often rise in value during inflation and act as a hedge.

Investing is the most powerful tool for building wealth over time.

Diversification:

Never put all your money in one place.

Diversifying reduces risk and stabilizes returns.

Risk is unavoidable — but manageable. Major financial risks include:

Successful investors manage risk, not avoid it.

Personal finance connects everything back to your daily life.

Every individual should have 3–6 months of emergency funds.

Even small amounts grow significantly over time.

Good debt builds assets (real estate, education).

Bad debt funds lifestyle consumption.

The financial world is changing faster than ever.

Fintech makes finance faster, cheaper, and more accessible.

AI enhances:

AI is redefining how decisions are made in finance.

Blockchain introduces:

Cryptocurrency represents a new era of digital assets.

Understanding modern finance is one of the most valuable skills in the 21st century. It empowers you to:

Finance is not just for bankers or economists — it’s for everyone. Whether you’re planning your personal budget, investing in the stock market, scaling your business, or trying to understand cryptocurrency, financial knowledge is your strongest advantage.