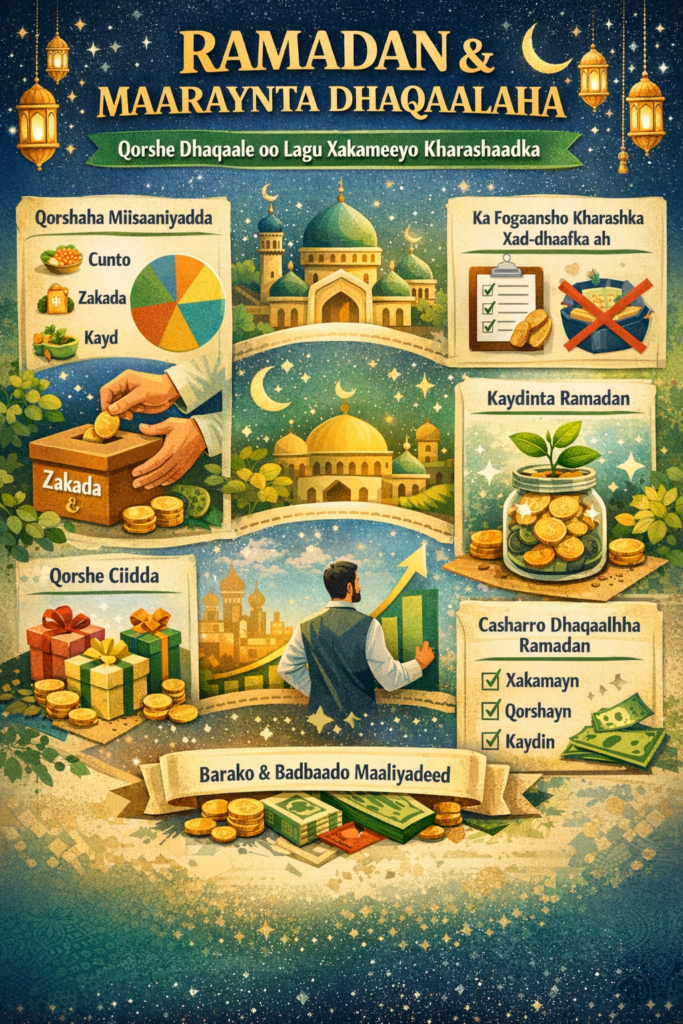

Baro sida loo maareeyo dhaqaalaha inta lagu jiro bisha Ramadan adigoo adeegsanaya xeelado maaliyadeed oo cilmi ku dhisan. Qorshe miisaaniyadeed, zakada, sadaqada, kaydinta, iyo ka fogaanshaha kharashaadka xad-dhaafka ah – dhammaan hal maqaal oo dhamaystiran.

Bisha barakaysan ee Ramadan waa waqti cibaado, naxariis, iyo isu naxariisasho. Laakiin sidoo kale waa waqti ay qoysas badan la kulmaan kordhin kharash, cadaadis miisaaniyadeed, iyo mararka qaar deyn lama filaan ah.

Anigoo ah qoraa iyo falanqeeye dhaqaale oo muddo dheer ku takhasusay maaraynta maaliyadda qoysaska iyo dhaqaalaha shakhsiyeed, waxaan maqaalkan kuugu soo bandhigayaa cilmi-baaris ku saleysan, xeelado la tijaabiyay, iyo talooyin wax ku ool ah oo kaa caawinaya inaad Ramadan ka dhigto bil lagu kordhiyo barako iyo hantiba – halkii ay noqon lahayd bil miisaaniyadda burburisa.

Cilmi-baarisyo badan oo lagu sameeyay dalalka Muslimiinta ah ayaa muujinaya in:

Arrintani waxay abuuri kartaa:

Haddaba su’aasha muhiimka ahi waa: Sidee loo maareeyaa dhaqaalaha Ramadan si xikmad leh?

U kala qaybi kharashaadka Ramadan 5 qaybood:

Tusaale ahaan:

| Qaybta | Boqolkiiba |

|---|---|

| Cunto | 40% |

| Zakada & Sadaqada | 20% |

| Dharka | 15% |

| Martigelin | 10% |

| Kayd | 15% |

Miisaaniyad la qorsheeyay ayaa ka hortagta kharash degdeg ah oo aan la fileyn.

Zakadu ma aha kaliya waajib diini ah, balse waa:

Dhaqaale ahaan, zakadu waxay kor u qaaddaa wareegga lacagta (money circulation), taasoo xoojisa suuqyada hoose.

Talo:

Ha sugina maalmaha ugu dambeeya. Qorshee zakadaada bil ka hor si aysan u noqon cadaadis degdeg ah.

Ramadan ma aha tartan cunto ama bandhig nololeed.

Cilmi-baarisyo muujinaya in qoysaska badankood ay iibsadaan cunto ka badan baahida, taasoo keenta:

Xeelado:

Dad badan waxay u arkaan Ramadan bil kharash oo keliya, laakiin waa fursad kaydin.

Sidee?

Haddii si sax ah loo qorsheeyo, waxaa suurtagal ah in 10–20% dakhliga la kaydiyo bishaas.

Waxaa jira fikrad khaldan oo leh:

“Ramadan waa bil kharash ah, ma aha bil maalgashi.”

Hase yeeshee, ganacsiyada qaarkood sida:

Waxay helaan koboc weyn.

Ganacsade caqli badan wuxuu Ramadan u arkaa:

Khaladka ugu badan waa in dhammaan lacagta lagu bixiyo Ramadan gudaheeda, kadibna Ciidda lagu galayo deyn.

Qorshe:

Ramadan waxay na baraysaa:

Dhammaan qodobadan waa mabaadi’da ugu muhiimsan ee guusha dhaqaale.

Maalmaha 1–5:

Samee miisaaniyad, xisaabi zakada.

Maalmaha 6–15:

Raac kharashaadkaaga, hagaaji haddii loo baahdo.

Maalmaha 16–25:

Hubi kaydinta iyo u diyaargarowga Ciidda.

Maalmaha 26–30:

Qiimee khibradaada maaliyadeed.

Ramadan waa bil barako, balse sidoo kale waa imtixaan maaliyadeed. Qofka qorshe leh wuxuu ka baxaa bisha isagoo:

Dhaqaalaha wanaagsan ma aha inta aad hesho – waa sida aad u maareyso.

Haddii aad rabto in Ramadan-kan uu noqdo mid dhaqaale ahaan kaa dhiga mid ka xoog badan sidii hore, bilow maanta – qorshee, xakamee, kaydi, maalgeliso.

Introduction: Why Personal Finance Matters More Than Ever

In today’s fast-changing world, personal finance is no longer a topic reserved for economists, bankers, or wealthy investors. It has become a daily survival skill for everyday people. From managing monthly expenses to planning long-term financial security, understanding how money works directly affects the quality of our lives.

Rising living costs, unstable global markets, inflation, digital currencies, and online financial tools have changed how people earn, spend, save, and invest money. Many people work hard every day, yet still struggle financially—not because they don’t earn enough, but because they were never taught how to manage money intelligently.

This guide was created to solve that problem.

At Dhilaalo.com, we believe personal finance should be simple, practical, and accessible to everyone—regardless of income level, education, or background. This article breaks down complex financial concepts into clear, real-world strategies that everyday people can apply immediately.

By the end of this guide, you will understand:

How to control your money instead of chasing it

How to build a realistic budget that actually works

How to save consistently, even on a low income

How investing works and how beginners can start safely

How to reduce financial stress and move toward long-term freedom

—

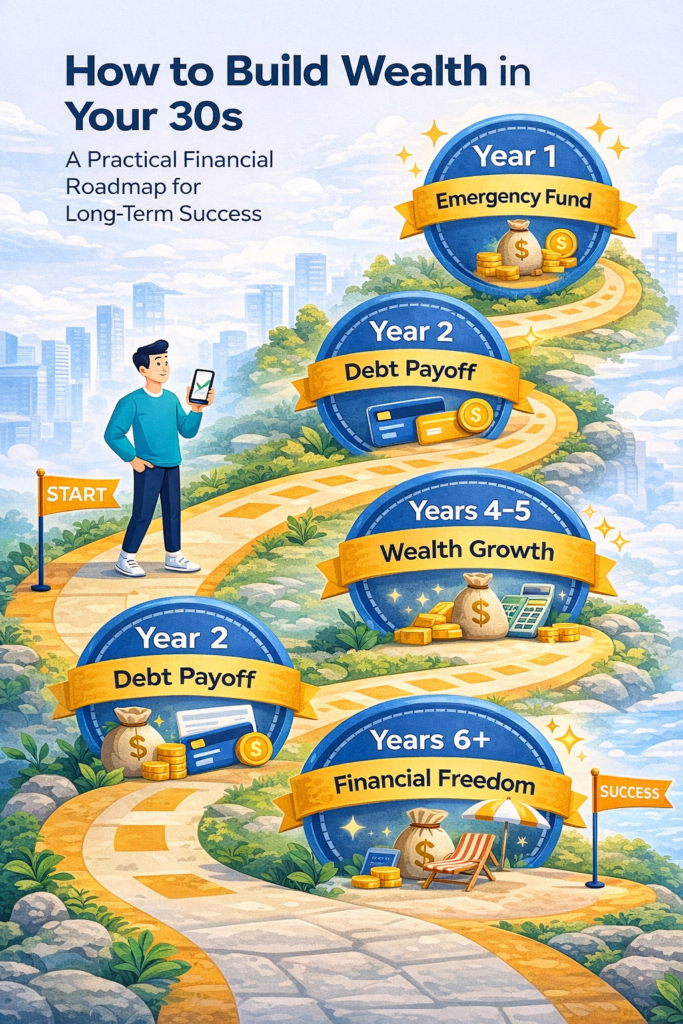

Introduction

Your 30s are one of the most powerful decades for building long-term wealth. You may be earning more than before, gaining career stability, or starting a family. But at the same time, expenses increase, responsibilities grow, and financial mistakes can become more costly.

The good news?

With the right strategy, your 30s can set you up for financial freedom in your 40s and beyond.

This guide breaks down clear, realistic, and proven steps to help you build wealth from where you are—without hype, risky shortcuts, or unrealistic promises.

—

1. Understand Your Financial Starting Point

Before building wealth, you must know exactly where you stand.

Key things to review:

Monthly income (after tax)

Fixed expenses (rent, utilities, insurance)

Variable spending (food, entertainment)

Total debt (credit cards, loans)

Current savings and investments

Create a simple net worth calculation:

> Net Worth = Assets − Liabilities

This number gives you clarity—not judgment. Wealth building starts with awareness.

—

2. Build a Strong Emergency Fund First

An emergency fund is the foundation of financial stability.

Why it matters:

Prevents debt during emergencies

Protects investments from early withdrawal

Reduces stress and financial anxiety

How much should you save?

3–6 months of essential expenses

Keep it in a high-yield savings account

Easy access, but not easy spending

This fund is not an investment—it’s insurance for your financial life.

—

3. Eliminate High-Interest Debt Aggressively

High-interest debt is one of the biggest obstacles to wealth.

Focus on:

Credit cards

Payday loans

High-APR personal loans

Two proven methods:

Debt Avalanche: Pay highest interest first

Debt Snowball: Pay smallest balance first for motivation

Paying off high-interest debt gives you a guaranteed return—often better than any investment.

—

4. Invest Early and Consistently

Time is your greatest asset in your 30s.

Best long-term investment options:

Index funds (S&P 500, Total Market)

ETFs with low expense ratios

Retirement accounts (401(k), IRA, Roth IRA)

Key principles:

Invest monthly (dollar-cost averaging)

Focus on long-term growth

Avoid emotional trading

You don’t need perfect timing—you need consistency.

—

5. Maximize Retirement Accounts

Retirement investing is not optional—it’s essential.

Smart steps:

Contribute enough to get employer match

Increase contributions with every raise

Prioritize tax-advantaged accounts

Why it works:

Tax benefits compound over decades

Employer match = free money

Automatic investing builds discipline

The earlier you invest, the less you need to contribute later.

—

6. Increase Your Income Strategically

Saving alone won’t build wealth—you must grow income.

High-impact income strategies:

Improve high-value skills

Negotiate salary every 1–2 years

Build online income (blogs, freelancing, digital products)

Invest in income-producing assets

Your income is your wealth engine. Focus on scalable growth.

—

7. Avoid Lifestyle Inflation

As income increases, spending often rises faster.

Wealthy people do this differently:

Maintain simple lifestyle

Increase investments before spending

Spend intentionally, not emotionally

Ask yourself:

> “Does this purchase move me closer to financial freedom?”

Control lifestyle inflation, and wealth accelerates.

—

8. Protect Your Wealth with Insurance

Risk management is part of wealth building.

Essential coverage:

Health insurance

Term life insurance (if dependents)

Disability insurance

Basic liability protection

Insurance protects your progress from setbacks you can’t predict.

—

9. Build Multiple Streams of Income

Relying on one income source is risky.

Examples:

Dividend-paying investments

Content websites (like Dhilaalo.com)

Affiliate marketing

Rental income

Digital assets

Multiple income streams create stability and faster growth.

—

10. Think Long-Term and Stay Disciplined

Wealth is built through habits, not luck.

Long-term mindset:

Avoid get-rich-quick schemes

Focus on systems, not shortcuts

Review finances quarterly

Stay patient during market cycles

Small consistent actions over time create extraordinary results.

—

Common Mistakes to Avoid in Your 30s

Waiting too long to invest

Ignoring retirement planning

Living paycheck to paycheck despite higher income

Taking excessive investment risks

Copying others without a plan

Avoiding mistakes is just as important as making smart moves.

—

Conclusion

Building wealth in your 30s is not about perfection—it’s about direction.

If you:

Control spending

Eliminate high-interest debt

Invest consistently

Increase income

Stay disciplined

You create a financial future that gives you freedom, security, and choices.

Start where you are. Improve one step at a time.

Your future self will thank you.

—

Introduction: Building Wealth Is Possible — Even from Zero

Many people believe that building wealth is only for those who start with money, high incomes, or special opportunities. That belief is wrong.

The truth is:

> Wealth is built through habits, systems, and long-term thinking — not luck.

This guide is written for beginners who are starting from zero and want a clear, realistic, and proven path to financial stability and long-term wealth.

Whether you earn a little or a lot, this guide will help you understand:

How money really works

How to avoid common financial traps

How to grow wealth step by step

—

1. Understand What “Wealth” Really Means

Wealth is not:

Buying expensive things

Looking rich

Making quick money

Wealth is:

Financial security

Freedom of choice

Control over your time

Assets that work for you

True wealth grows quietly and consistently.

—

2. Master Your Money Mindset First

Before money grows in your bank account, it must grow in your mind.

Key mindset shifts:

From “I don’t earn enough” → “How can I manage what I have better?”

From “Money is stressful” → “Money is a tool”

From “I’ll start later” → “I start now”

Your mindset determines:

How you spend

How you save

How you invest

—

3. Know Exactly Where Your Money Goes

You cannot build wealth if you don’t know:

How much you earn

How much you spend

Where your money leaks

Action Step:

Track every expense for 30 days:

Rent

Food

Transport

Subscriptions

Small daily spending

This alone can change your financial life.

—

4. Build an Emergency Fund First

Before investing or taking risks, protect yourself.

Why an emergency fund matters:

Prevents debt

Reduces stress

Gives confidence

How much?

Start with $500 – $1,000

Then aim for 3–6 months of expenses

Keep this money:

Safe

Accessible

Separate from spending money

—

5. Eliminate High-Interest Debt

High-interest debt is the enemy of wealth.

Focus on:

Credit cards

Payday loans

Personal loans with high interest

Strategy:

1. Pay minimums on all debts

2. Attack the highest interest debt first

3. Avoid creating new debt

Every dollar of debt paid is a guaranteed return.

—

6. Live Below Your Means (Without Suffering)

Living below your means does not mean living poorly.

It means:

Spending intentionally

Avoiding lifestyle inflation

Choosing value over appearance

Wealthy people often:

Drive affordable cars

Delay gratification

Invest the difference

—

7. Start Saving Automatically

Saving should not depend on willpower.

Best system:

Pay yourself first

Automate savings

Treat savings like a bill

Even:

$10/day

$50/week

$100/month

…compounds over time.

—

8. Invest Early — Even with Small Amounts

Time is more powerful than money.

Beginner-friendly investments:

Index funds

ETFs

Retirement accounts

Long-term stock investing

Key rules:

Invest consistently

Think long-term

Ignore short-term noise

You don’t need to be rich to invest — investing makes you rich.

—

9. Increase Your Income Strategically

Saving alone is not enough.

Ways to grow income:

Learn high-value skills

Freelancing

Online businesses

Passive income streams

Focus on:

Skills that scale

Income that grows over time

—

10. Protect Your Wealth

Wealth without protection disappears.

Protect through:

Insurance

Diversification

Avoiding scams

Continuous education

—

11. Stay Consistent and Patient

Wealth building is boring — and that’s good.

There will be:

Slow months

Market drops

Doubts

But consistency always wins.

—

Conclusion: Wealth Is a System, Not a Secret

You don’t need:

Perfect timing

Huge income

Special access

You need:

Discipline

Knowledge

Time

Start small. Stay consistent. Think long-term.

> Wealth from zero is not a dream — it’s a process.

I

n 2025, the economy continues to evolve rapidly, and many people are seeking additional income streams to keep up with inflation, cover expenses, and build long-term wealth. Side hustles offer more than just extra cash—they can help you gain new skills, explore potential business opportunities, and achieve financial security.

Benefits of side hustles:

This guide outlines the best side hustles in 2025, from online to offline opportunities, beginner-friendly to advanced, helping you pick the right one for your lifestyle and goals.

Freelancing remains one of the most flexible and lucrative side hustles. You can work from home or anywhere, and set your own schedule.

Estimated earnings: $500–$3,000/month depending on experience and hours worked

Online education continues to expand in 2025, making tutoring and online courses highly profitable.

Estimated earnings: $20–$60/hour for tutoring, $500–$5,000/course (passive income potential)

If you have a blog, YouTube channel, or social media following, affiliate marketing can generate passive income.

Estimated earnings: $100–$5,000/month depending on traffic and conversions

Selling physical or digital products online can provide a scalable income stream.

Estimated earnings: $200–$2,000/month

Part-time gig work such as ride-sharing and delivery is still relevant in 2025.

Estimated earnings: $300–$1,500/month

Investing small amounts consistently can grow into a substantial secondary income.

Estimated earnings: $50–$1,000/month initially, growing over time

Monetize creativity through art, photography, or digital content.

Estimated earnings: $100–$2,000/month depending on portfolio and marketing

Offline opportunities remain lucrative for community-based work.

Estimated earnings: $300–$2,500/month depending on demand

Make your existing assets work for you.

Estimated earnings: $200–$3,000/month depending on asset and location

Short-term, high-demand work can boost income.

Estimated earnings: $300–$1,500 per season

Choosing the best side hustle in 2025 depends on:

Pro tip: Start with one or two side hustles, track income and effort, then expand. Multiple income streams reduce financial risk and accelerate wealth building.